During the post-COVID-19 pandemic period of 2020, many countries experienced relatively high inflation. This reflects two factors:

1. All countries have been hit by shocks such as coronavirus-related supply chain disruptions and the war in Ukraine.

2. Most countries enacted very large economic stimulus programs, with similar effects in each case.

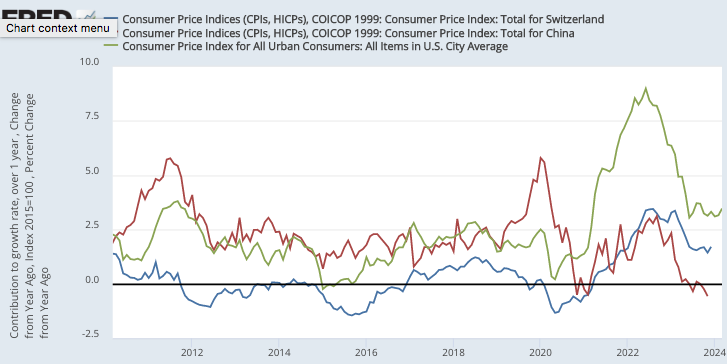

It was appropriate to allow some increase. inflation Responding to negative supply shocks. This is the whole idea behind “flexible” average inflation targeting. However, actual inflation rates also reflected excessive aggregate demand growth and were disproportionately high in many countries, including the United States. I’m concerned that people seem to be suggesting that the Fed could not have done anything, since spikes in inflation are occurring in many other countries as well. In fact, not all countries experienced extremely high inflation. Note that China (red line) and Switzerland (blue line) saw some inflation increases, but much lower than in the United States (green line).

in podcast Along with David Beckworth, former Fed Vice Chairman Richard Clarida says the similar pattern experienced by most countries suggests that differences in monetary policy regimes were not important in this particular case. Suggests.

The most important thing to remember about the lessons learned from the post-pandemic inflation surge is that they were very similar across countries, implementation settings, and policy strategies. In other words, inflation was too high for a single-mission inflation target like the Bank of England. Inflation was too high for the eurozone, which has inflation targeting as its only mandate.

Inflation was too high in Switzerland. It was too expensive in Australia. It was too expensive in Canada. Furthermore, with the exception of the SNB and Norway’s central bank, all other developed country inflation targeters also took a reactive path in that they did not start raising interest rates until core inflation in their countries was well above target. . . So there was something about the initial conditions, that the inflation rate was too low for 10 years. In terms of the size and complexity of the shock, it affected both demand and supply, which is why central banks did something very similar and had very similar lift-offs. , a very similar history of inflation, and now very similar disinflation.

So I think that as time goes on, scholars will look back at this period and not think that it has revealed too much about inflation targeting versus flexible average inflation targeting, single mandate versus dual mandate. and predict. They think it will reveal something about the initial conditions and the magnitude and complexity of the shock.

I argue that the cross-national patterns I see suggest that some policy regime differences are more important than others. For example, consider the case of China. The inflation rate has fallen to a level that is even lower than Japan’s, and in fact to just below zero. Why did this happen?

It is worth noting that the Japanese currency has recently depreciated very sharply against the US dollar, while the depreciation of the Chinese currency has been very small.Several critic China has signaled its reluctance to allow a sharp depreciation of its currency for fear of provoking a protectionist reaction in the United States. Whatever the reason, China appears to have resorted to excessively tight monetary policy because it does not want to allow its currency to suffer a significant drop in foreign exchange value.

this is, money price approach The policy approach can be much more powerful than the interest rate approach, a point I highlighted in a recent book. Once China decided not to allow a sharp depreciation of its nominal exchange rate, it could now achieve an equilibrium real exchange rate only by allowing price level deflation. A similar pattern occurred in Argentina in the late 1990s. At this time, the combination of a fixed exchange rate and a strong US dollar caused price deflation.

PS. Nothing in Clarida’s interview makes me optimistic about the upcoming review of the Fed’s policy regime. At the very least, I think it’s clear that the average inflation targeting regime needs to be made symmetric, but I don’t see Fed officials advocating for such a change. I hope I’m wrong, but I’m expecting the same thing: policy “rules” that allow too much discretion.