IR_Stone

Even though AI hype has propelled many software stocks to new highs this year, many of their former highs remain underwater. Snowflake (New York Stock Exchange:snow) is a great example. Cloud data warehouse companies have been struggling all year due to slowing growth. growth rate.

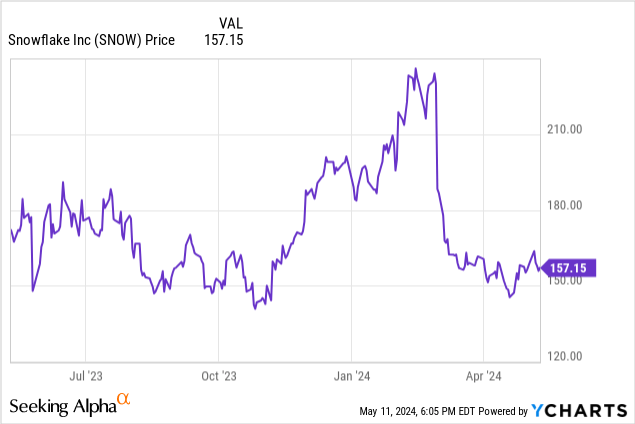

Since the beginning of the year, Snowflake stock has fallen nearly 20%. The stock remains down more than 50% from its pandemic-era high of just under $400, once one of the most popular trades in the tech sector. As we look ahead to Snowflake’s all-important Q2 earnings release scheduled for May 22, the question we must ask ourselves is: Does Snowflake have room to recover?

The last time I wrote a neutral opinion on Snowflake was in February of this year, downgrading my previous bullish view when the stock was still trading. Close to $240. Since then, the stock has plummeted following disappointing fourth-quarter results that showed customer growth and a sharp slowdown in net revenue retention.

The truth here: Enterprise purchasing patterns remain low as IT departments balance the need for budget cuts with upfront purchases to support AI and automation. Despite what appears to be a tailwind from an increase in generative AI workloads, Snowflake remains a victim of its own scale, resulting in slower growth.

Amid all these negative factors, I’m downgrading Snowflake again despite the stock price decline since the beginning of the year. bearish As we await the company’s first-quarter earnings release on May 22nd, we recommend selling this stock before another disappointing quarter brings Snowflake’s stock price further down.

Negative readthrough from other high growth software companies

Snowflake reports its first quarter results relatively late in the earnings season, so it has the advantage of being able to read the results of other similar companies.

In my opinion, one of the best public stock comps for Snowflake is Palantir (PLTR). Although Palantir’s big data mining software is neither adjacent nor competitive to Snowflake’s cloud data warehousing products, I view both companies as similarly sized, large-cap software stocks that are still growing rapidly. ing.

Unfortunately, Palantir fell ~10% after earnings. The main issue was the company’s second quarter guidance, shown below.

Palantir Outlook (Palantir Q2 Earnings Release)

The midpoint of Palantir’s guidance, $651 million (up 22% year-over-year), was one point below Wall Street’s estimate of $653 million (up 23% year-over-year). The key point here is: Although Palantir technically had a beat-and-raise quarter, and its outlook for the quarter didn’t suggest a slowdown, the Street still left the stock depressed. This reflects the fact that valuations have been gradually increasing and a high interest rate environment leaves little margin for error beyond perfect results and guidance.

Palantir isn’t the only software stock to fall by double digits this fiscal year. Data Dog (DDOG) also fell more than 10% on its own earnings report last week. Although the outlook for this quarter is slightly above street expectations..

Olivier Pommer, CEO of Datadog, said: Datadog’s recent first quarter earnings report Over the past week, we’ve seen usage patterns normalize, although budget constraints continue to be a major theme for some customers.

So let’s talk about the business drivers for this quarter. The first quarter saw greater usage growth from existing customers than the fourth quarter, and this first quarter usage growth was on top of that experienced in the second and third quarters of 2022. It was similar. As a reminder, this period saw usage normalize following the accelerated growth we experienced in 2021. Overall, we saw healthy growth across our product lines. And as always, our new products grew at a faster rate on a smaller base.

Some customers remain cost conscious, but the intensity of their optimization efforts has decreased. As an example, the optimization cohort we identified a few quarters ago continued to grow this quarter. We also see our customers adopting more products and our usage increasing. ”

Both Datadog and Snowflake rely on usage-based revenue models. Snowflake usage trends have gotten worse lately, so I’m hoping to see some of the normalization/improvements we’re seeing with Datadog. Still, Snowflake has struggled against high expectations backed by similarly high valuations.

Moderate trend heading into Q1

Moving away from some of the companies in Snowflake in the first quarter, we have to keep in mind that Snowflake itself is trending weaker heading into the first quarter.

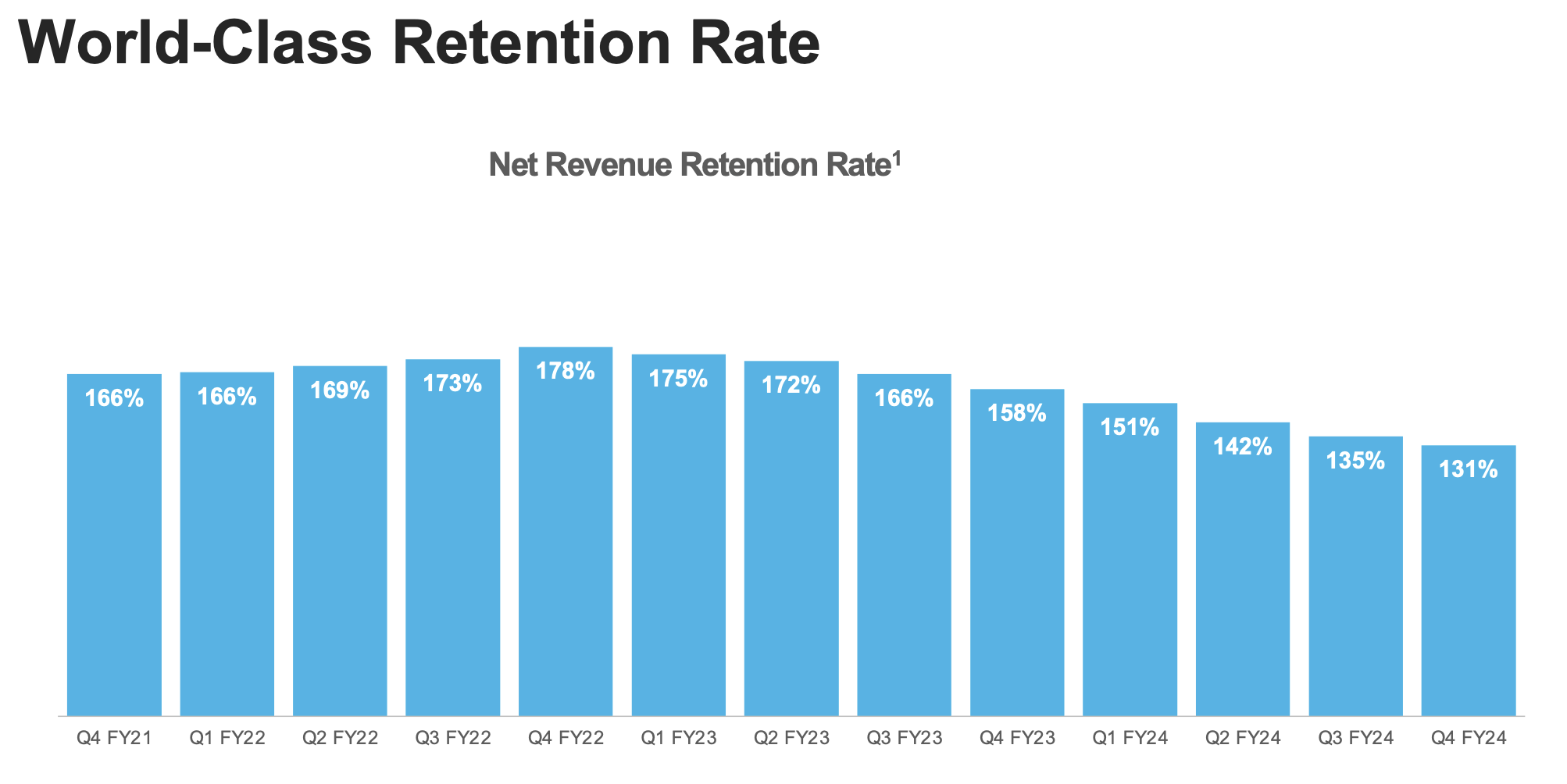

Note from the company’s fourth quarter results that Snowflake’s net revenue retention rate, which is a function of customer usage and spending habits, continues to decelerate.

Snowflake Retention Trends (Snowflake Q4 Earnings Deck)

As shown in the graph above, retention rates peaked in the fourth quarter of 2022 and have slowed for eight consecutive quarters.

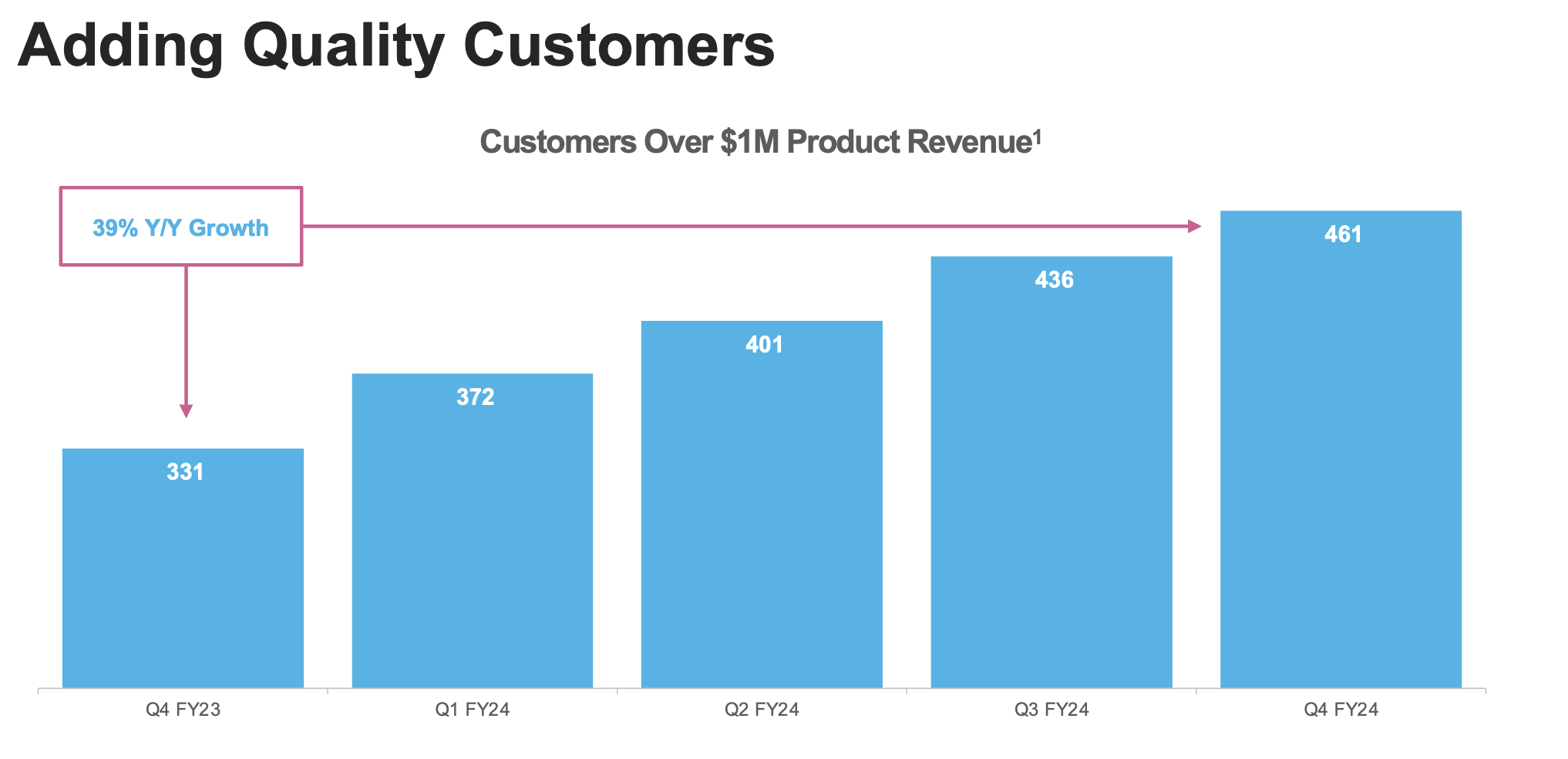

Additionally, Snowflake’s ability to add large customers has also slowed. The number of customers with annual revenue over $1 million fell from 35 in the third quarter to 25 in the fourth.

Snowflake Customer Trends (Snowflake Q4 Earnings Deck)

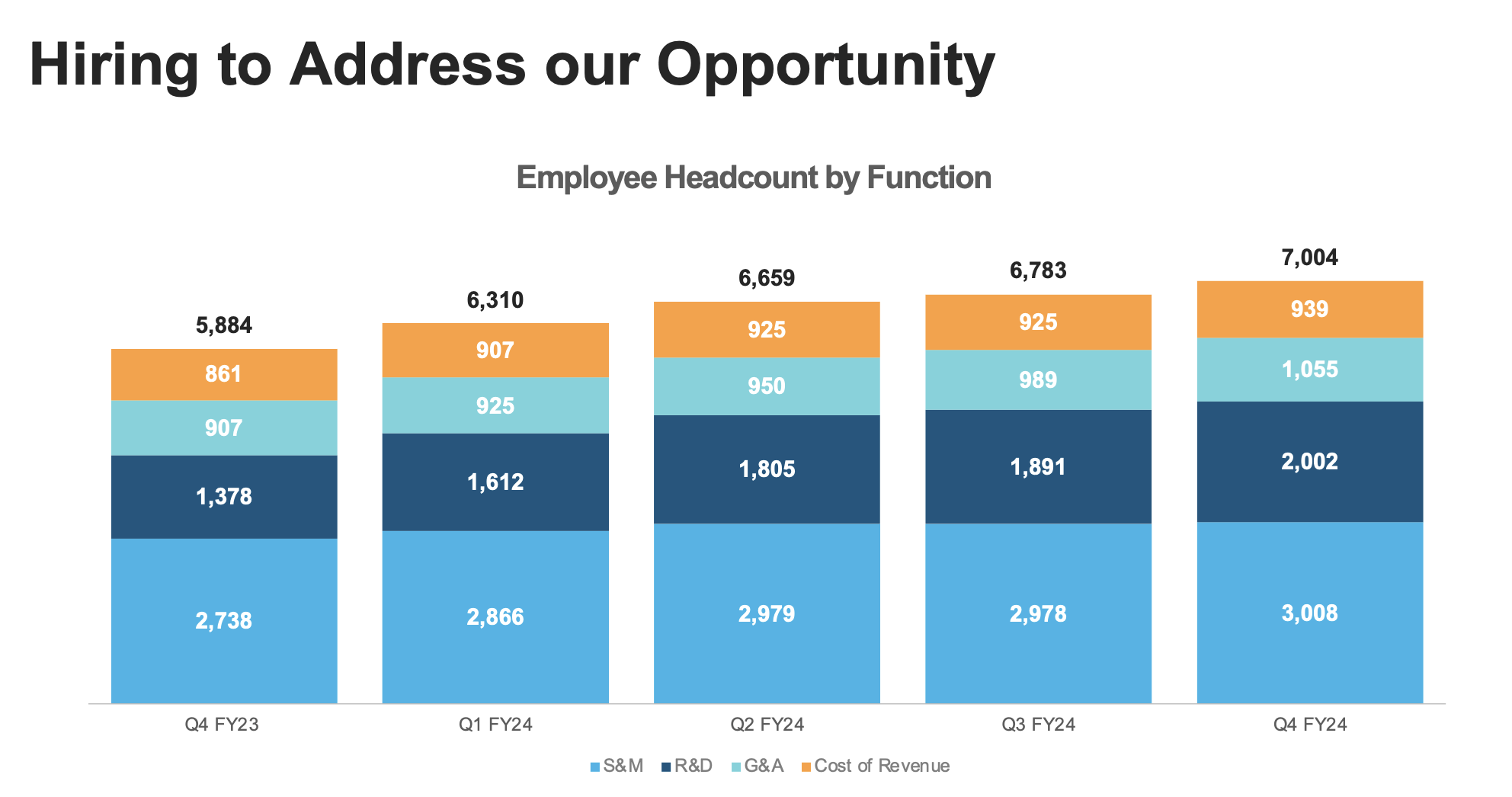

Revenue growth has slowed to the low 30s over the past two quarters, compared to more than 50% growth in Q1 FY24. Also note that Snowflake has limited his FY25 product revenue growth to 22% year over year. But despite this growth slowdown, the company, like many of its peers, has completely avoided large-scale layoffs. In fact, the company continues to grow its workforce, hiring more than 200 new employees in the fourth quarter alone.

Snowflake Employee Count (Snowflake Q4 Earnings Deck)

It’s worth noting that Snowflake’s guidance calls for pro forma operating margins of just 6%, 2 percentage points worse than FY24. This reflects steady operating profit growth amid slower revenue growth.

Evaluation and important points

With sales slowing, expenses rising and margins shrinking, and readings from other software companies not giving us much confidence in strong results, there’s little reason to continue investing in Snowflake through earnings.

Despite these risks, stock prices are by no means cheap. The current stock price is just over $150, giving the company a market capitalization of $52.52 billion. After subtracting his $4.76 billion in cash on Snowflake’s most recent balance sheet, the company’s results are: Corporate value is $47.76 billion.

Snowflake’s consensus revenue forecast is $3.43 billion for FY25 (up 22% YoY) and $4.23 billion for FY26 (up 23% YoY). 13.9x EV per FY25 revenue and 11.3x EV per FY26 revenue – High double-digit valuation multiple for a software company whose growth is expected to slow into the 20s. Unlike software peers that deploy SaaS business models, Snowflake’s revenue is do not have Because it is recurring, it can be highly volatile depending on usage (which is why it has a lower valuation compared to its SaaS peers).

I would be more eager to buy Snowflake if the stock price fell below. $120, target price representing EV/FY26 revenue multiple 8.5x Up to 20% downside from current levels. In my view, Snowflake could end up there soon due to weak earnings. Watch this stock carefully. But don’t buy before it drops further.