D-Keine/E+ via Getty Images

Investment Thesis

Palo Alto Networks, Inc. (Nasdaq:Pan W) shares fell nearly 30% after the company released its third-quarter fiscal 2024 earnings. I believe this massive sell-off may be justified due to the high expectations for the company. Generative AI is expected to be a revenue driver as shares rose 170% in February from their 2023 lows. Previous articleIn 2018, I initiated a Buy recommendation and discussed the company’s sustainable path to achieving the Rule of 40 amid slowing revenue growth. Since then, the stock has risen more than 40%.

The company maintained its Rule of 40 in the last quarter, approaching 40% despite solid demand. My biggest concern is that weak billing guidance and mid-teens revenue growth will severely hinder FCF growth. Meanwhile, the stock continues to trade as if it is a high-growth software company. In the past, the stock has traded higher, so I’ve downgraded the stock from a buy to a neutral rating due to the stock’s expensive valuation amid slowing growth. In particular, the price-to-earnings ratio is now expensive compared to a year ago.

The rule of 40 is still valid

Corporate Model

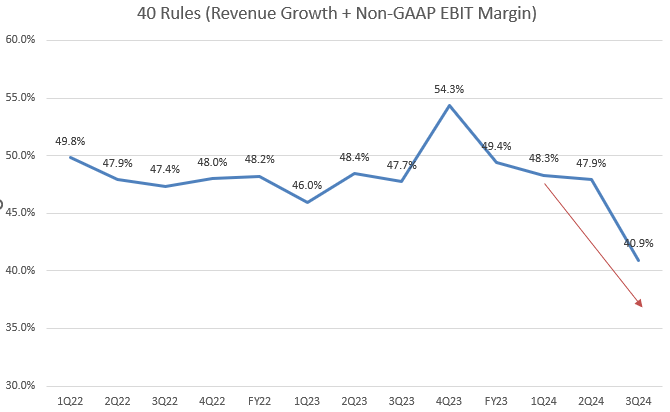

While PANW achieved the Rule of 40 with a headline rate of 40.9% (revenue growth + non-GAAP EBIT margin) last quarter, the trendline has turned downward, dropping below the 45% threshold for the first time since Q1 FY22. We attribute this decline primarily to weakening top-line growth. Specifically, subscription and support revenue grew 20% year-over-year, down from 29% year-over-year growth in Q3 FY23. However, we are encouraged to see relatively strong growth in the subscription revenue segment, up 25% year-over-year.

In press releaseThe company expects fourth-quarter fiscal 2024 total sales to grow 10-11% year over year, approaching “single digits.” Given the stock’s reaction last week, CRM PerformanceI think there is anecdotal evidence that it could disrupt investors’ psychological thresholds and lead to increased volatility going forward.

Continued profit growth

Corporate Model

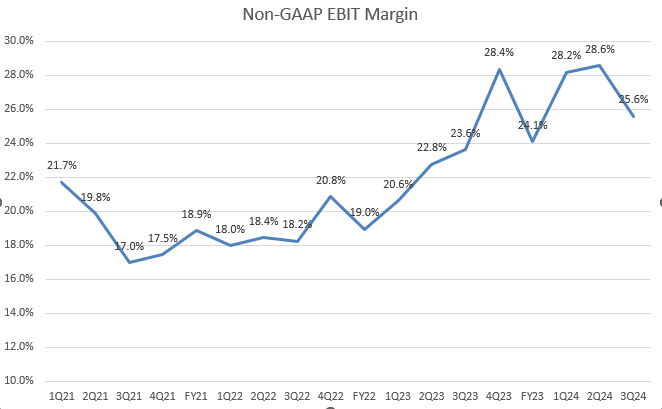

Additionally, the company’s profit margins remain strong, which is a positive sign. It is common for a company’s profit margins to expand as revenue growth slows. However, it should be noted that some investors may no longer view PANW as a high-growth stock, which could impact its current premium valuation. With many SaaS companies positioned to be beneficiaries of Generative AI, investors are eager for a re-acceleration of growth and increased demand to be reflected in earnings reports. However, some of these software companies have disappointed investors in recent earnings seasons.

Significant slowdown in sales growth

Corporate Model

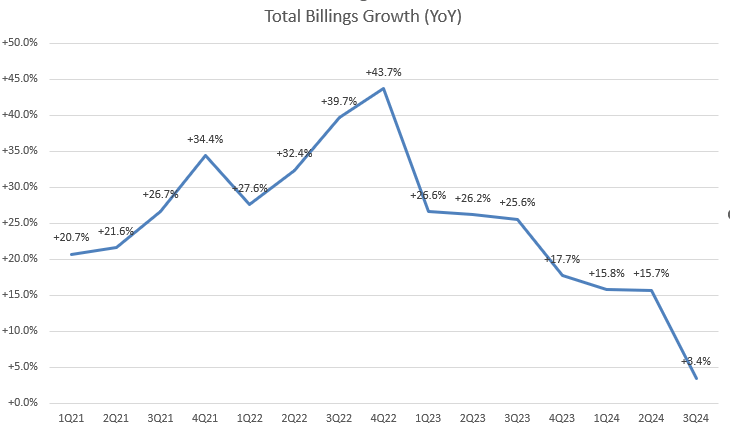

Let’s take a look at the chart. Billings Cash liquidity plays a key role as a key growth driver for FCF, which, unlike earnings, reflects the actual cash flow a company receives in a given period of time. In our previous article, we highlighted the company’s impressive sales growth. However, total sales growth slowed to 3.4% YoY in the third quarter of fiscal 2024. Notably, current sales growth slowed to single digits, growing 8% YoY for the first time in the company’s history.

In terms of guidance, the company expects 9.5% YoY growth in Q4 FY2024 and 10.5% YoY growth in FY2024, which is significantly lower than its +20% YoY growth rate. Earnings Report The company explained that “Faced by high cost of funds, more customers are choosing to defer payments over the purchase period rather than paying upfront, leading to an increase in large transactions.” It also expects this trend to continue. Continued deferred payments will create significant headwinds for cash flow generation and FCF margins in the future. Typically, FCF growth has plummeted from 40% YoY in Q3FY23 to 14% YoY in Q3FY24. Therefore, it expects that the company may suffer from negative FCF growth in the coming quarters.

However, PANW’s order book is progressing well. This suggests that demand for the company’s AI products is increasing, as evidenced by a 20% YoY increase in current order book for Q3FY24 versus a 15% YoY increase for Q3FY23. This is primarily due to a 20% YoY increase in current remaining performance obligations (cRPOs). RPOs indicate contract commitments that a company needs to fulfill at a later date. These backlogs turn into future billings, which ultimately help generate revenue. While management has emphasized the importance of focusing on RPOs and order book, I believe it would be a red flag for PANW if both revenue and FCF growth slowed.

evaluation

J.P. Morgan

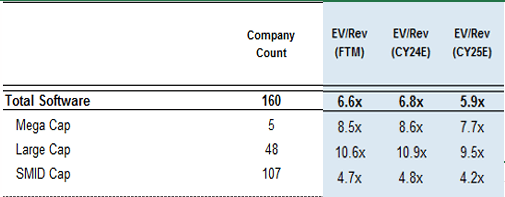

PANW is currently trading at 53x non-GAAP P/E FTM, even after a 20% decline from its February peak. That’s nearly double the Nasdaq 100 Index’s P/E FTM of 27.5x. Meanwhile, its EV/Sales FTM is currently at 11.7x, above the large software average of 9.5x. I know it’s not a perfect comparison, but many investors are looking at NVIDIA’sNVDA) has “skyrocketed” over the past 12 months. But NVDA’s non-GAAP P/E FTM is just 41x, still cheaper than PANW.

Moreover, PANW’s current non-GAAP P/E FTM is roughly in line with its five-year average of 54.3x. Although revenue growth has slowed significantly from +25% in FY2023 to a forecast of 16% in FY2024, the multiple remains roughly the same. This explains the optimistic outlook for growth reaccelerating under Generative AI trends. Therefore, I prefer to remain on the sidelines until we have more clarity on revenue growth for AI security services.

Conclusion

In conclusion, buying PANW low after its recent offering may not be wise, as the company’s recent earnings results have failed to live up to the high expectations and prior rally surrounding generative AI. While PANW has maintained a growing backlog, the continued downward trend in revenue growth is of concern and could cause PANW to fall out of the Rule of 40 club in the coming quarters. The significant slowdown in billing growth and conservative forward guidance also raise questions about future FCF growth. While margins and orders remain healthy, I believe the slowdown in revenue and FCF growth raises concerns about the current valuation multiple. Moreover, PANW’s multiple still looks expensive compared to the industry average and companies such as NVDA. Therefore, I am downgrading the stock to Neutral to reflect these concerns. I believe the current valuation already factors in potential AI growth tailwinds.