Art Wager/iStock Unreleased via Getty Images

introduction

I have a portion of my investment portfolio in bonds, but am still looking for additional investments in preferred stocks. As interest rates in the financial markets fall, The price of fixed-rate preferred stock will rise (assuming the issuer’s creditworthiness remains unchanged). Preferred Stock in Sunstone Hotel Investors Co., Ltd. (New York Stock Exchange:Sho) a few months ago at a temporary price surge and I’m wondering whether I should re-establish a long position.

First quarter results and outlook for the year

When I look at preferred stocks, I look at two things: preferred dividend coverage and asset coverage — in other words, how safe are the preferred dividends and how safe are the preferred stocks.

SHO Investor Relations

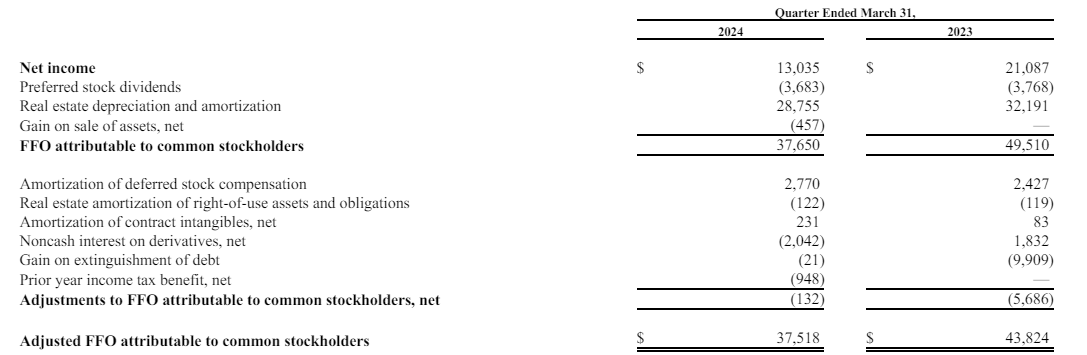

In the first quarter of this year, Sunstone Hotel Investors reported net income of $13 million, but since net income for a REIT is relatively meaningless, I wanted to take a look at how Sunstone’s FFO and AFFO were performing. As shown below, FFO attributable to common shareholders totaled $37.7 million, which, after making small adjustments, was: AFFO was down just $100,000 to $37.5 million..

SHO Investor Relations

Based on an average share count of 202.6 million shares in the first quarter, AFFO per share was approximately $0.18, down compared to $0.21 in the first quarter of 2023, which would put 2024 on track to be relatively weak overall.

That’s because portfolio redevelopment plans are underway and Sunstone plans to spend $135 million to $155 million on capital expenditures. While the bulk of the impact will be felt in the coming quarters, these investments should pay off handsomely in 2025. Sunstone aims to use short-term pain to unlock long-term gains.EBITDA increase of $20-22 million in 2025.

Looking at its full-year guidance (see below), Sunstone expects total AFFO to be between $171 million and $192 million, and AFFO per share should be between $0.84 and $0.94. This includes the impact of remodeling some assets.

SHO Investor Relations

Considering that AFFO of $182 million (the midpoint of current guidance) already includes preferred dividends of $14.7 million for the year, AFFO before preferred dividends would be approximately $197 million, for a preferred dividend payout ratio of just under 8%, excluding the impact of capital expenditures this year.

How does this affect preferred stock?

Currently, there are two series of preferred stock: Explained in the previous article;

The H series is (New York Stock Exchange:Show PRH) under its ticker symbol and offers a 6.125% preferred dividend of $1.53125 per annum. Meanwhile, the I Series is (New York Stock Exchange:Show PRI) under its ticker symbol and offers a preferred dividend of 5.7% with annual payments of $1.425. Both issues are cumulative and can be called by Sunstone beginning after May 2026 (SHO.PR.H) and July 2026 (SHO.PR.I).

Both preferreds rank equally, so you end up buying the one with the highest yield (because you think the risk of the preferreds being called is negligible), which is why looking at the current yield makes more sense than looking at the call yield, since you think the chances of it being called are pretty low.

Find Alpha

Based on Thursday’s closing prices, H shares are trading at $21.30 and I shares are trading at $20.24, yielding 7.2% and 7.04%, respectively. That means that based on the current share price, Series H appears to be the better option due to its higher preferred dividend yield.

The balance sheet still looks healthy. As shown below, the REIT has just $980 million in total debt, but it has $471 million in cash and restricted cash. Excluding restricted cash, net debt is just $414 million, compared with $2.59 billion in total assets (already Accumulated depreciation: $1.16 billion).

SHO Investor Relations

The REIT’s next quarterly update will likely see a hit to its cash position due to Sunstone’s recent acquisition. Hyatt Regency San Antonio Riverwalk – $230 millionHowever, this represents just 11.1 times estimated 2024 EBITDA. 12.5 times NOIThis acquisition Will increase in future.

Investment Thesis

I sold both series of preferred stock in March of this year when Series I was trading at over $21 per share and Series H was trading at over $23 per share. Currently, Series H is trading at just $21.30, which represents a significant improvement in yield compared to the price at which I sold my position.

Sunstone Hotel Investors does not offer the highest yield in the sector, but I believe it offers the safest preferred dividend yield given the portfolio’s very low LTV ratio. I am seriously looking at preferred shares again, and if I were to re-establish a buy position, it would be in the highest yielding series.