Al-Qsam

Overview of EMB

iShares JP Morgan USD Emerging Markets Bond ETF (Nasdaq:EMB) is designed to provide exposure to US dollar-denominated debt issued by emerging markets. US-based investors tend to prefer US dollar-denominated exposure. Reduces currency risk.

From an emerging market perspective, they see this as an opportunity to tap into demand, and therefore will fund much of their issuance with US dollar-denominated bonds. These two factors have given the ETF a sizeable scale, with expected net assets of over $14 billion. EMB website.

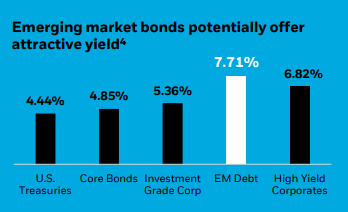

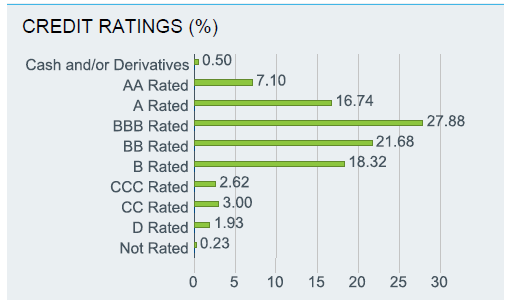

Investing in emerging market bonds may seem risky, but the ETF’s extreme diversification mitigates some of the risk. EMB Product OverviewMore than 50 government agencies and more than 600 Fixed income, over half of which are investment grade. This mix has generally delivered portfolio yields to maturity above 7% this year.

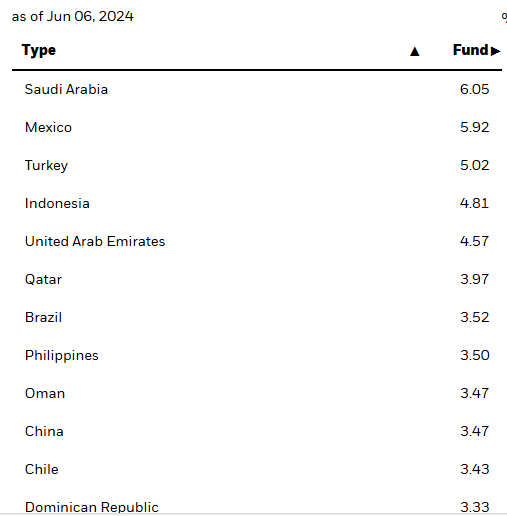

The ETF pays monthly distributions and had less than 6% exposure to its largest countries as of the end of March this year — for example, exposure to Saudi Arabia, Mexico, Turkey and Indonesia was around 5% to 6% at that time.

When considering where EMBs fit into the fixed income universe, it is helpful to keep in mind this snapshot from data at the end of March this year:

EMB product overview using Bloomberg yield data as of 31/03/2024.

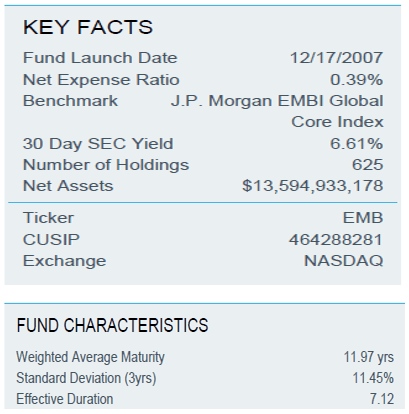

EMB Fund Details

Something else notable about this ETF is that it has an average maturity of almost 12 years, with an effective duration of over 7 years, so to get such a high yield, you are taking on a fair bit of risk in terms of sensitivity to interest rate movements.

The drawdown observed in 2020 is also notable in terms of risk in a “risk-off” market environment, which we examine in the chart below.

This ETF has a modest fee of 39bps, whereas an actively managed emerging market bond fund would likely have fees in excess of 1%. Whether this is “cheap”, however, comes down to a debate about whether active managers add value after fees, a debate we will address later in this article.

EMB Factsheet 31 March 2024.

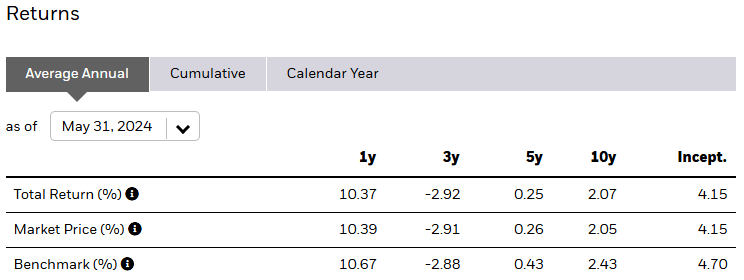

EMB Performance History

Performance figures since inception (December 2007) are set out in the table below.

EMB website, data as of 31 May 2024, start date 17 December 2007.

These performance figures are certainly not inspiring, but in fairness, this is primarily a period during which we have faced what many have described as a structurally low yield environment for global fixed income. It is only in 2022 that this has really changed.

Emerging market bonds’ current high yields and improved performance over the last year could provide even more reason to invest now, as global inflation fears in 2022 have eased somewhat.

Analysis by EMB Colleagues

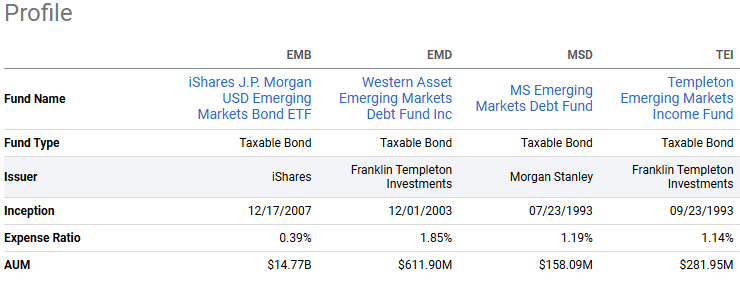

When comparing EMB to other similar funds, we thought it would be useful to consider the following points.

EMB Fund Comparison, Seeking Alpha.

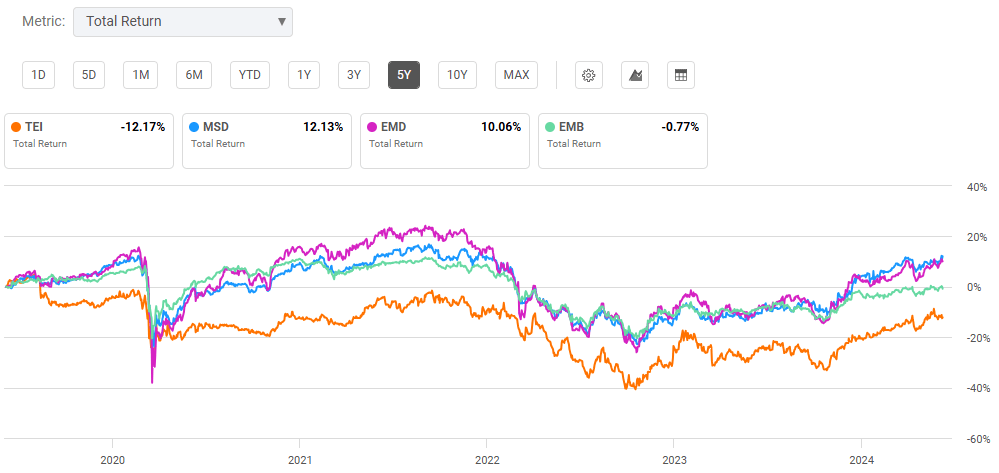

There are three closed-end funds out there, and while I understand they are looking to deliver higher yields, there are a few reasons to consider such alternatives: These funds are benchmarked to the JP Morgan USD EMBI Global Index, but they take on aggressive investment risk and typically run portfolios with lower average credit ratings compared to the EMB.

From that perspective, we expect that such CEFs will likely perform better over the long term. When considering alternatives, it’s important to keep in mind their respective volatility in recent years.

Total returns for the five-year period ending June 7, 2024, Seeking Alpha.

While EMB has outperformed one of the CEFs above, it has clearly lagged behind the other two over the past five years. Because this represents total returns, it incorporates fluctuations in the CEFs’ NAV discounts over the period. However, such fluctuations are relatively modest, so analyzing the above performance solely on NAV return data would show a similar conclusion.

This highlights that relying on active managers can always be hit or miss, but it does provide food for thought as to whether a passive product like EMB is a good fit for this asset class.

What is the difference between active and passive management of emerging market debt?

Templeton Emerging Markets Income Fund ETF (NYSE:TEI), MS Emerging Markets Bond Fund ETF (NYSE:MSD) and Western Asset Emerging Markets Bond Fund (NYSE:EMD) has regularly traded at double-digit discounts to NAV in recent years. It charges significantly higher fees than EMB, but Active management is preferred in emerging countries.

Naturally, the above article was written by an active manager. Nevertheless, the compelling arguments that active is better than passive are specific to emerging market debt. So just because you think you can use passive with U.S. stocks, you shouldn’t impose a simple conclusion that passive is better.

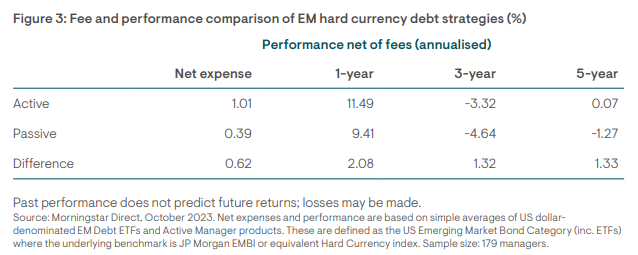

In reference to the research I linked to in the paragraph above, I found the following table interesting: Even if I accept that looking at the past 5 years is never a conclusive indicator of future performance, it’s still worth knowing – meaning that in hindsight, paying the “expensive” active manager fees was probably a better option.

Morningstar Direct Research, October 2023, via ninetyone.com

Regarding the CEF mentioned above, earlier this year MSD reviewed This was my favorite pick in this category, although I would argue that EMD isn’t far behind.

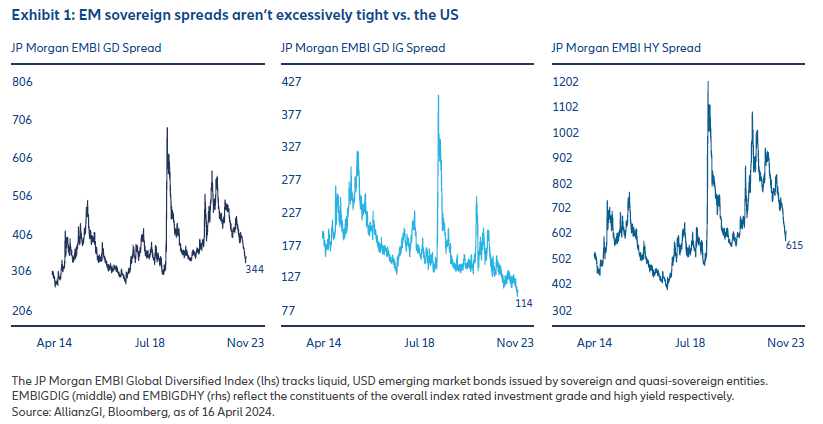

Emerging market sovereign bond spreads are not so attractive

If we look at some charts over the past decade, we can see that emerging market bond spreads have tightened significantly over the last few years.

AllianzGI, Bloomberg data, as of April 16, 2024

While the spreads are not depicted as “excessively tight” on the charts, I don’t find them all that attractive given that they are still significantly tighter than they have been in the past decade.

Emerging market bond funds have continued to perform well since mid-April, when the spread data in the chart above was updated, and with potential risks looming, now may be a good time to lock in some of the big gains of the past year.

If the past decade has been any indication, the global macroeconomic environment is becoming more risky. Most economists expect similarly robust global growth to continue next year, but relatively tight emerging market debt spreads seem to be pricing in a “Goldilocks” type of economic environment. This comes at a time when “sticky” inflation and rising geopolitical risks continue to dominate the headlines.

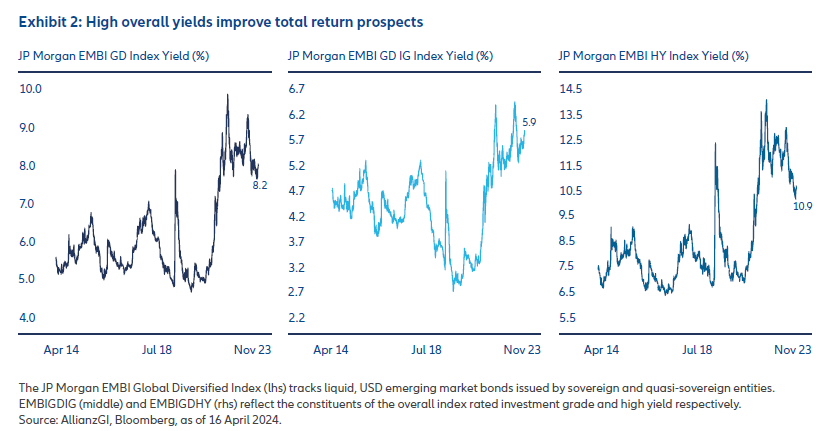

Emerging market bonds offer high yields across the board, but inflation remains high

Below are three 10-year charts of the same emerging market bond index, but displayed in yields.

Morningstar Direct Research, October 2023, via ninetyone.com

As I mentioned earlier, from a nominal return perspective, future return prospects look brighter than they have for most of the past decade. Of course, we hope so, given that the ETF has only returned about 2% per year over that period.

But even if EMBs do make a big improvement on the poor returns of the past decade, they will still need to beat the expected rise in inflation over the next decade. If inflation remains “sticky,” the higher yields offered by emerging market bonds may not be worth the risk.

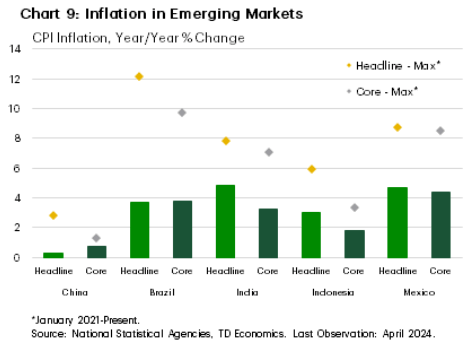

by TD Economics Inflation TrackerThe tendency for inflation to become sticky has also been observed in major emerging market economies. To quote TD: Inflation rates across major emerging markets have fallen significantly from their peaks (Figure 9), but improvement has slowed in recent months.. “

National statistics agency, TD Economics, data from January 2021 to April 2024.

Will upcoming Fed rate cuts be a boon for emerging market bonds?

You may be reading the question above and wondering why this is phrased as if it is a certainty, but that is exactly what I am trying to say. Over the past year, there has been a lot of discussion about choosing investments to benefit from upcoming Fed rate cuts. At the same time, however, those anticipated rate cuts continue to be postponed into the coming months.

Emerging market bonds are one example of an asset class that many investors are betting will benefit from a Fed rate cut, potentially leading to a weaker US dollar. On the other hand, a stronger US dollar could be problematic for emerging markets, as it makes it more expensive to service debt that is raised in US dollars.

A weaker US dollar also often correlates with improved global risk appetite, an environment in which emerging market debt spreads are expected to tighten further.

Emerging market bond spreads have already tightened significantly over the past few years, making it a bit worrying for holders of emerging market debt to look forward to a weaker U.S. dollar.

Investors who believe the US dollar will weaken may also consider investing in local currency emerging market bonds. An example of a way to gain exposure is the iShares JP Morgan EM Local Currency Bond ETF.NYSEARCA:LEMB)

Over the past year, the LEMB has underperformed the EMB during periods when the US Dollar has been stronger than expected.

One-year total returns through June 7, 2024, Seeking Alpha.

Exposure to top EMB countries

Data from EMB website, June 6, 2024.

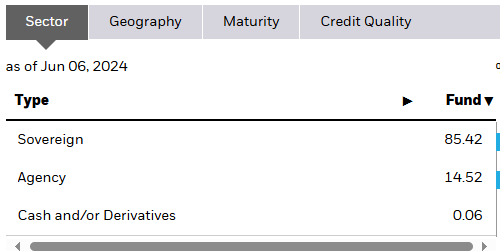

EMB Sector Allocation

Data from EMB website, June 6, 2024.

EMB Exposure by Credit Rating

EMB factsheet, data as of 31 March 2024.

Conclusion

If you’re looking for a fund that will deliver relatively high monthly income, I would avoid EMB for now. EMB finally delivered solid returns last year, helped by tightening emerging market spreads, but now seems the time for holders to lock in profits.

It remains unclear whether global central banks, including those in emerging markets, will be able to say goodbye entirely to inflation fears from 2022. The highly anticipated Fed rate-cutting cycle, which many investors hope might boost sentiment among emerging market central banks and others, is also looking increasingly uncertain.

In addition to the uncertain geopolitical environment, the past few weeks have seen Unpredictability in emerging nation politics.

For those who prefer to maintain some core exposure to this asset class, actively managed CEFs such as MSD and EMD may produce better returns over the long term.