JHVE Photo

Marvel Technology (Nasdaq:MRVRMarvell is a leading supplier of data center infrastructure semiconductor solutions for the data center core and network edge. Marvell’s data center business accounted for more than 70% of its recent total revenue. quarterMarvell expects AI revenues from optics and custom ASICs to reach over $1.5B by FY25. Additionally, the company is poised to expand its data center switching portfolio (active electrical cables) in the near future. I initiate with a “Buy” rating with a one-year price target of $80 per share.

The growth of AI optics and custom silicon

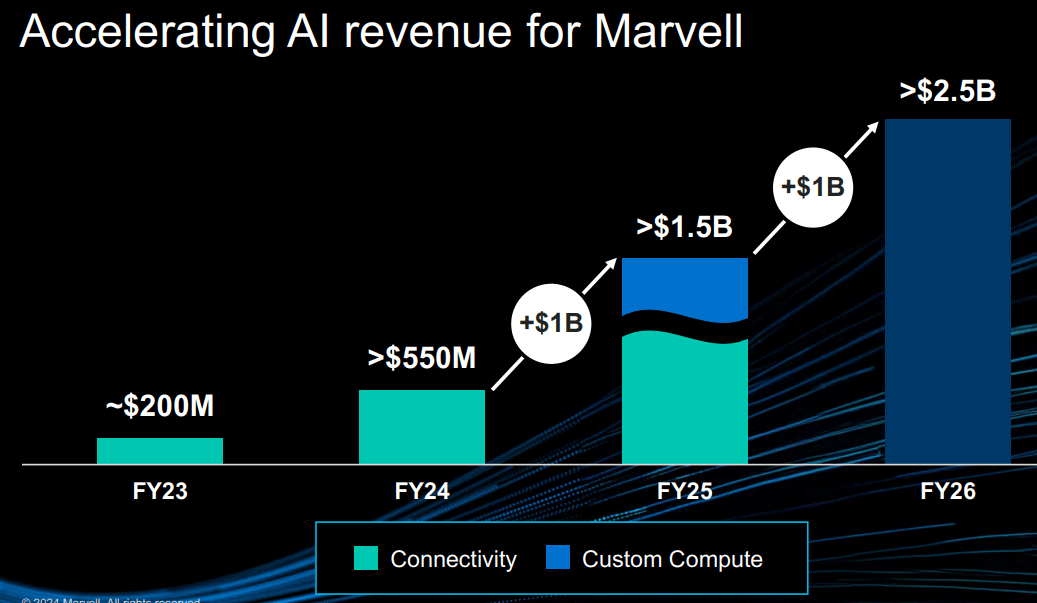

Marvell’s AI efforts are in its data center optics and custom silicon (“ASIC”) businesses, and the company expects to generate over $1.5 billion in revenue from AI by FY25, as shown in the chart below.

Marvel Investor Presentation

- AI Optics: Marvell’s Optical Portfolio This includes Pulse Amplitude Modulation, Digital Signal Processors, Laser Drivers, Transimpedance Amplifiers and Data Center Interconnect Solutions. Data centers require interconnect solutions to connect GPUs, routers and switches at scale. Marvell is well poised to capture the rapid growth of the data center interconnect market.

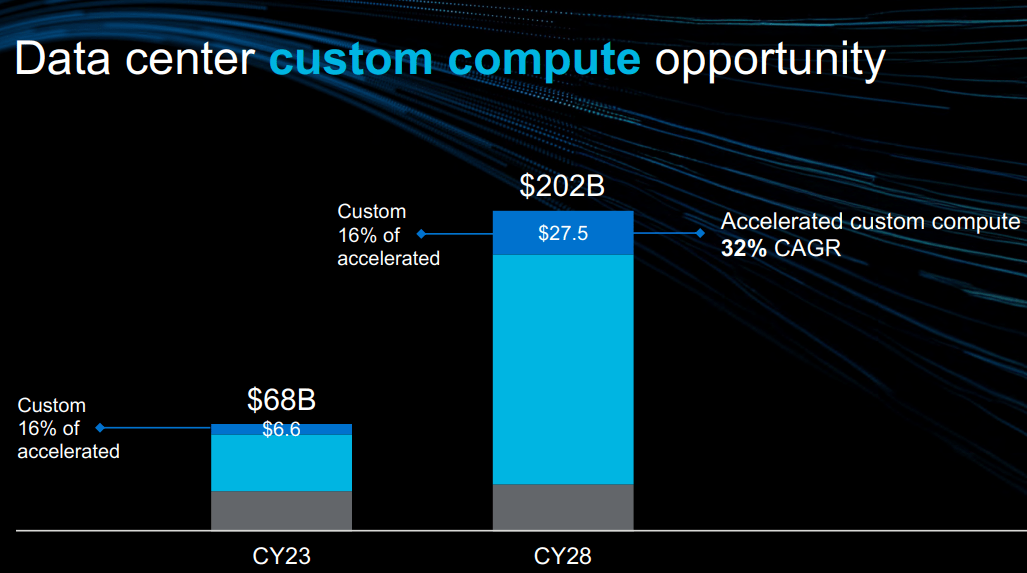

- Custom ASICs: The company develops system-on-chip solutions for individual customers. For example, MicrosoftMSFT),Amazon(Amazon) and alphabet (Google) can purchase standard GPU products from Nvidia orNVDA), AMD (Am), or Intel (International Trade Commission), or they could use Marvell’s ASIC technology to design their own chips. Marvell is working with all the hyperscalers to design their own chips, according to executives. Business InsiderMarvell holds around 15% share of the custom ASIC market. Marvell has helped manufacture Amazon’s 5nm Tranium chips and Google’s 5nm Axion ARM CPU chips. Additionally, Marvell is evolving 3nm technology with these hyperscalers. As shown in the slide below, the total addressable market for custom ASICs is expected to grow at a CAGR of 32% from FY23 to FY28, driven primarily by the rapid growth of AI and datacenter.

Marvel Investor Presentation

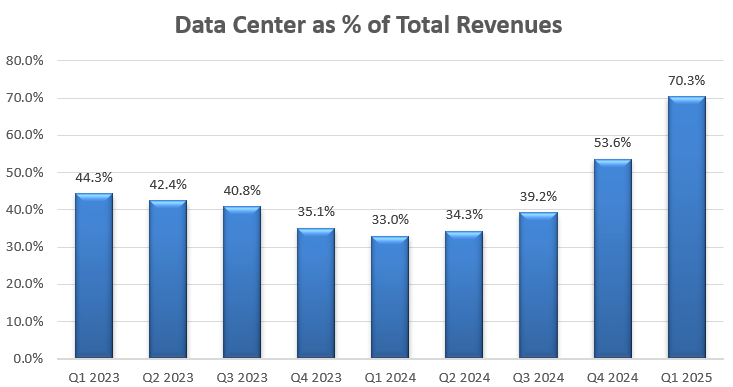

With AI currently growing rapidly, Marvell expects its optical and custom ASIC businesses to grow rapidly over the next few years. As shown in the chart below, Marvell has significantly grown its data center business over the past few quarters, accounting for over 70% of its total revenue in 2015. 1st Quarter of FY25.

Marvel quarterly results

Weakness in other cyclical businesses

Marvell makes up 30% of its revenue from several cyclical businesses, including enterprise networking, carrier infrastructure, consumer electronics, and automotive markets. In the first quarter of fiscal 2025, enterprise networking revenue was down 58% year over year, carrier infrastructure was down 75%, consumer was down 70%, and automotive/industrial market revenue was down 13%.

A high interest rate macro environment has enterprises and telcos cutting IT budgets. Additionally, CIOs need to prioritize AI spending within limited IT budgets. These macro headwinds have led to temporary weakness in the enterprise, telco, automotive, and industrial markets.

Over the long term, we expect these cyclical businesses to continue to grow, albeit at a slower pace than our data center business. Announced 100G/lane Active Electrical Cables (“AEC”) enable 400G, 800G, and 1.6T server-to-switch and switch-to-switch solutions. Marvell’s Ethernet controllers and network adapters are likely to continue to grow along with the enterprise Ethernet market. That said, these cyclical businesses may continue to pose headwinds in the near term.

Recent performance and outlook for FY2025

Marvel is 1st Quarter of FY25 The company released its financial results on May 30, reporting a 12.2% decrease in revenue and a 21.8% decrease in net income, primarily due to significant declines in its 5G, automotive/industrial, enterprise networking, and carrier businesses, as mentioned above.

What impressed me most about the quarter was the strong growth in our data center business, up 87% year over year and up 7% sequentially. Earnings ReportManagement expressed optimism about growing demand for AI applications. The company has begun initial deployments of custom AI computing silicon with hyperscalers. It expects revenue contribution from custom ASICs to start in FY25.

The company expects its second-quarter revenue to increase 8% sequentially, driven primarily by strong growth in data centers.

Marvel Investor Presentation

The following factors are taken into consideration for FY2013:

- Data Center: Given Marvell’s strong Q1 growth, we expect its data center business to grow 70% in FY25, driven by both its interconnect and custom ASIC businesses. It’s worth noting that Marvell generated just $2.2 billion in revenue from data center in FY24, so the base from which its interconnect and custom ASIC businesses can grow rapidly is small.

- Enterprise Networking and Carrier Infrastructure: End markets are currently experiencing inventory correction, but markets are likely to normalize and recover in the second half of FY25. Conservatively, we expect Marvell’s revenues to decline 40% in FY25.

- The automotive semiconductor market is normalizing after the pandemic. S&P Global Global new vehicle sales are expected to grow 2.8% year-over-year in 2024. The automotive division is a small part of Marvell’s business, accounting for less than 7% of total revenue. Marvell expects revenue to grow 3% in FY25.

All things considered, Marvell’s revenue is expected to grow 7.3% in FY25.

evaluation

To project normalized revenue growth beyond FY25, I consider the following:

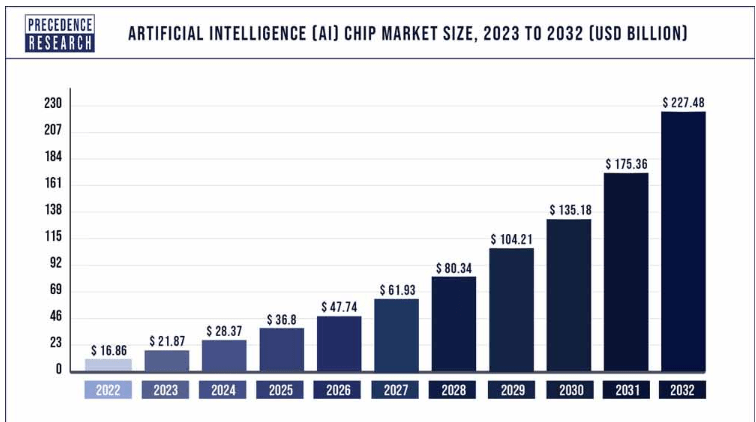

- Data Center: I’m bullish on Marvell’s custom silicon and AI optics businesses. Precedence Research Predict The AI chip market is expected to grow at a CAGR of 29.72% from 2023 to 2032. Given the rapid adoption of AI by enterprise customers and hyperscalers, Marvell expects its data center market to grow at a CAGR of over 30% from FY25 onwards.

Previous research

- Enterprise Networking and 5G: The market has historically grown at mid-single digit rates. Enterprise customers will need to invest in edge networking to deploy AI training and inference workloads in the future. Marvell expects its business to grow 5% annually.

- Automotive chips: ON Semiconductor (upon) and NXP Semiconductors (NXPI), the automotive semiconductor market is expected to grow by more than 12% in the future, so Marvell believes it will be well placed to grow in line with market growth in the near future.

As a result, Marvell expects revenue to grow 16% annually in FY25 and beyond.

In April 2021, Marvel Acquisition The company acquired Inphi, a leader in high-speed data interconnection platforms for the data center market, for $10 billion. In retrospect, this was a great acquisition and contributed greatly to Marvell’s current technological advancements in the data center market.

In addition, Marvel Inobium In August 2021, Marvell completed acquisitions aimed at accelerating networking solutions for cloud and edge data centers. These acquisitions have caused Marvell to incur significant amortization charges over the past few years, with annual amortization exceeding $1 billion. In fiscal 2023, Marvell still has $4 billion of intangible assets on its balance sheet, and I believe acquisition amortization charges will begin to gradually decline in the near future, contributing to the company’s margin expansion opportunities.

I expect Marvel’s operating expenses to grow 13.5% annually, leading to earnings expansion of 360 bps per year.

Additionally, the company assumes that it will allocate 10% of total revenue to M&A, contributing to 3.3% growth in sales. Here is a summary of the DCF model:

Marvell DCF – Author’s calculations

Free cash flow from equity is calculated as follows:

Marvell FCFE – Author’s calculations

The cost of equity capital is calculated to be 17%, assuming a risk-free rate of 4.2%, a beta of 1.88, and an equity risk premium of 7%. Discounting all future FCFE, the one-year target price is calculated to be $80 per share.

Main risks

Circular business: Marvell is a semiconductor company and operates in a highly cyclical industry. In the near term, its 5G, enterprise networking, automotive, and industrial businesses are in a down cycle. In the longer term, we expect Marvell’s revenue growth to remain volatile and investors should prepare for quarterly fluctuations.

Exposure to ChinaChina accounts for 43% of total revenue, exposing Marvell to risk of potential regulatory activity, including tariffs, export controls and sanctions. The outcome of the U.S. presidential election could also affect Marvell’s exposure to export controls.

Expansion of stock-based compensation plans: Marvell spent 11.1% of total revenue on stock-based compensation (SBC) in FY24, up from 9.3% in FY23. As a semiconductor company, Marvell’s SBC expenses are quite high. Management needs to manage SBC expenses appropriately going forward.

Conclusion

I value Marvell’s leadership position in the AI optics and custom ASIC markets and believe the company’s business is highly relevant, especially as demand for data centers and AI computing grows. I initiate with a “Buy” rating with a one-year price target of $80 per share.