DenisTangneyJr/E+ via Getty Images

introduction

On May 28th I article title “My Favorite Things! 3 Stocks That Are Super Attractive to the Natural Gas-Fueled AI Boom”

The article was very long. Natural gas prices are bullish, supported by a massive increase in energy demand due to new AI applications.

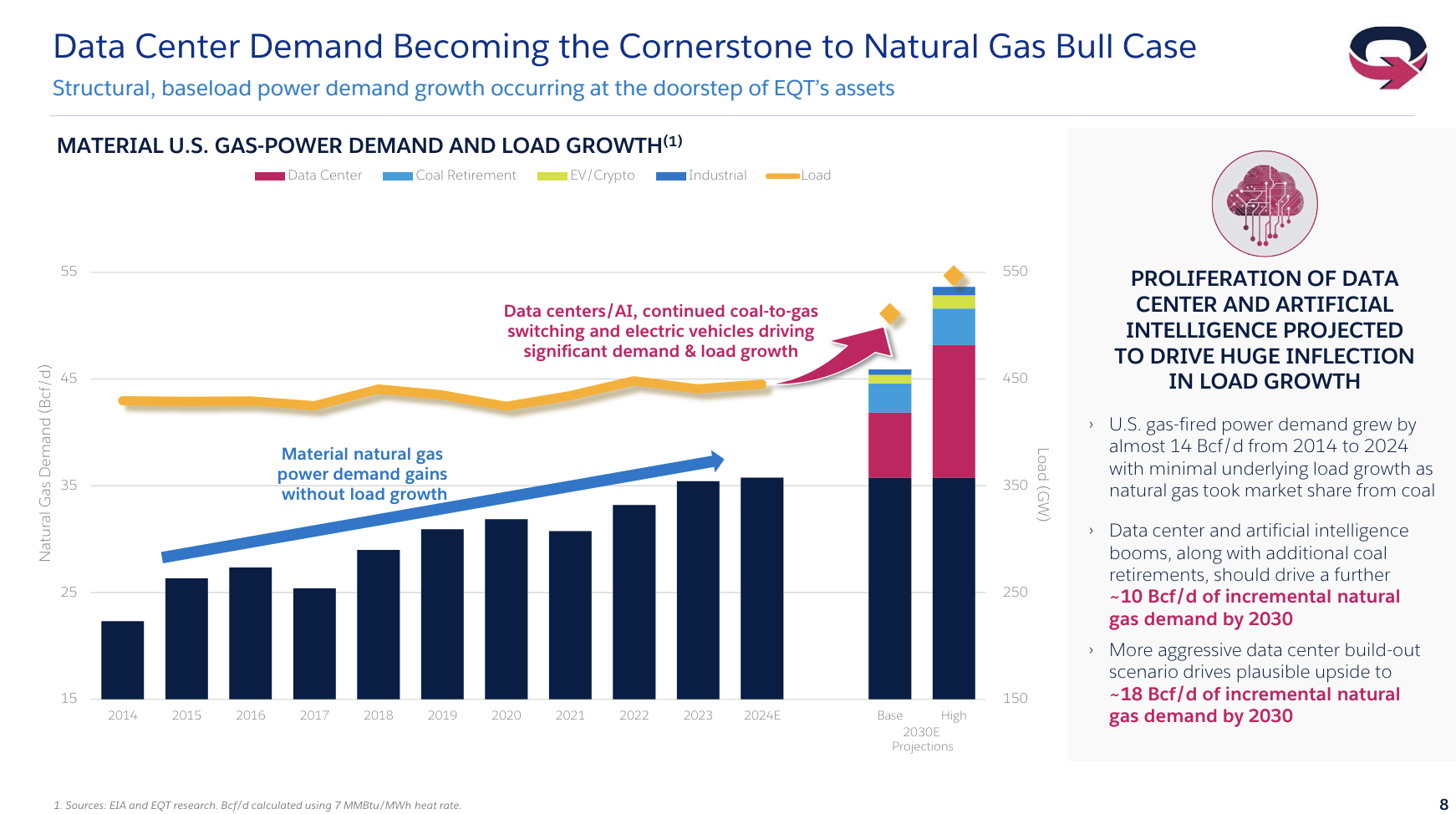

The report added that up to an additional 8.5 billion cubic feet of natural gas per day could be needed to meet growing demand.

(…) the report states: Current power demand from data centers is 11 gigawatts (GW)which is the base case Expected to grow to 42GW by 2030.

In the base case, the report states: An additional 2.7 billion cubic feet of natural gas will be needed by 2030.. – Reuters (emphasis added)

According to EQT: Co., Ltd(EQTAustralia, one of the world’s largest natural gas producers, is expected to see an increase in demand of 10 billion cubic feet per day by 2030 due to AI alone.

An even more bullish forecast calls for an increase of 18 billion cubic feet per day.

EQT Corporation

Again, this is solely due to AI.

Exclusions:

- World population growth.

- The growth of the middle class in emerging markets.

- The transition from coal to natural gas is underway.

Overall, export demand is very bullish.

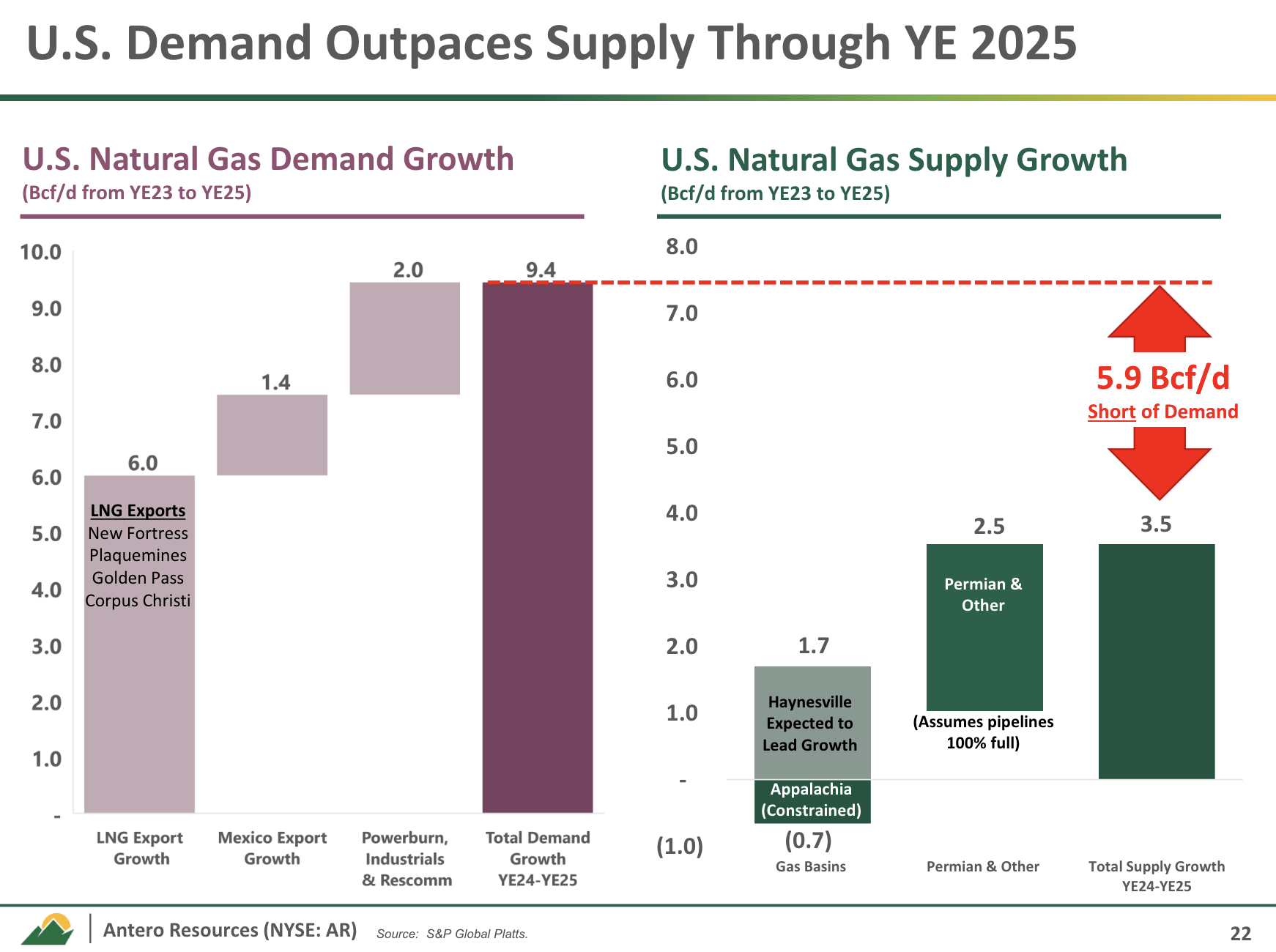

Antero Resources (New York Stock Exchange:AR)The company, which is the subject of this article, predicts that growing LNG (liquefied natural gas) exports will create 6 billion cubic feet per day of new demand by 2025. When adding in growing domestic demand and increased exports to Mexico, the company believes there will be a supply shortfall of about 6 billion cubic feet per day.

Antero Resources

This is a very bullish sign and is one of the reasons why natural gas prices have started to recover.

Prices have only just normalized for now, but the momentum we are witnessing is truly remarkable.

TradingView (NYMEX Henry Hub)

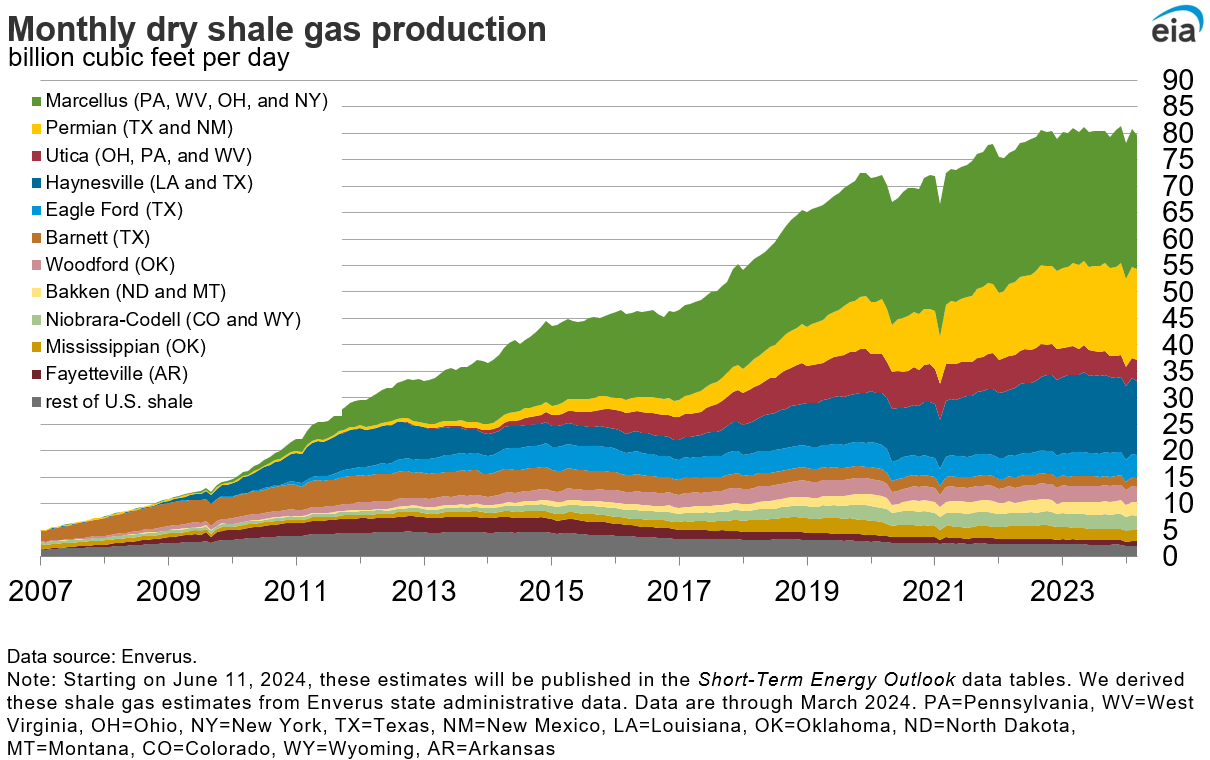

That being said, the supply side has changed overall as the United States has experienced an unprecedented increase in natural gas production due to the shale revolution.

Well, that’s done.

Natural gas remains extremely abundant (especially compared to oil), but production growth has slowed dramatically.

Energy Information Administration

In light of these changes, Goering & Rosenkweig Assert We could see a big shift in inventory, with North American prices converging to much higher international prices.

The US is on track to move from a long period of severe oversupply to a structural shortage of historic proportions. While inventories remain elevated, our models predict they will reach dangerous levels much sooner than anyone expects. Given this, it makes no sense to us that US natural gas is trading at a record discount to energy equivalent prices, even after two consecutive mild winters. Investors should take note.

In essence, the end of the shale revolution coincides with the fastest growth in natural gas demand in history.

Return to Goehring & Rozencwajg.

Although it is very early, we believe that less liquefied and less transported North American natural gas will converge to the world price, currently at $10 per million cubic feet. Investors are very bearish after two consecutive mild winters, but are ignoring the bullish shifts in both supply and demand that are underway. This is the most asymmetric investment we can remember.

This is where Antero Resources comes in.

Why I’m Bullish on Antero Resources

I’ve been bullish on Antero Resources since I began coverage in 2023.

My recent article On February 19th, I Strong Buy evaluation.

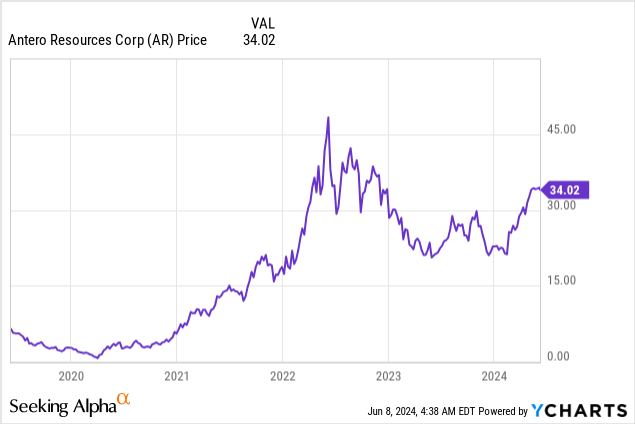

Since then, the stock has surged 43%, dwarfing the S&P 500’s 7% return.

I believe this is just the beginning, as AR has several characteristics that make it a great stock to profit from the natural gas bull market.

First, the company has been holding high-quality inventory in the Marcellus Basin (Appalachia) for over 20 years, making it one of the most efficient producers.

To be precise, excluding new developments, the company has 22 years of inventory below the breakeven point of $2.75/Mcfe (Henry Hub’s unit of measurement, 2.85 MMBtu).

Antero Resources

The company is very efficient within its basin.

For example, the company reduced drilling time per 10,000 feet to 5.4 days in the first quarter of this year, down from 5.5 days in 2023.

Additionally, Antero set a new record by completing an average of 11.3 stages per day, significantly less than the previous year’s figure of just under 11 stages per day.

Antero Resources

The company also improved on new completion technology, saving more than an hour of pumping time each day and helping Antero Midstreammorning) advanced water infrastructure will be introduced to alleviate congestion.

This infrastructure also eliminates the need for water tankers.

In general, we lead our peers in capital efficiency, requiring only $0.55 per Mcfe to maintain production, nearly double the peer average.

Antero Resources

On an unhedged basis, the company breaks even at 2.24 million cubic feet, which is better than its major peers, especially those in higher-cost basins like the Haynesville.

Antero Resources

On top of that, AR has another big advantage: product mix.

AR is a natural gas producer, but not all of the gas it produces is low-margin natural gas.

The company has a large footprint in the liquids and NGL (natural gas liquids) markets.

U.S. propane exports rose to a record high of more than 2.3 million barrels per day in the first quarter, a 14% increase over the 2023 average.

Antero Resources

This export growth and strategic pricing decisions have enabled Antero to sell its products at a premium price.

For example, propane prices averaged 44% as a percentage of WTI in early 2024. This is up from 36% in 4Q23.

In addition, Antero’s decision to sell the majority of its seaborne crude oil at international price bands rather than through domestic long-term trades positions the company to benefit from better international prices.

Antero Resources

My point is that AR is not a natural gas producer that is primarily dependent on Henry Hub prices within its basin.

Even better, the company is a major LNG player, selling about 75% of its natural gas from its own fields, primarily into the Gulf Coast LNG corridor.

As you can imagine, this puts the company in a great position to access higher prices and benefit from rapidly growing global demand for LNG.

According to the company’s own data, its peers sell just 13% of their capacity to the LNG corridor.

Antero Resources

In addition, there are three other major benefits:

- More than half of the company’s production is liquids.

- The company is the only major U.S. natural gas producer expected to sell natural gas at a price above Henry Hub.

- The company sells 100% of its natural gas from its own basins.

Antero Resources

I believe these attributes set the company apart as one of the best natural gas stocks on the market.

Shareholder benefits

In addition to having a great business model, the company has been aggressively reducing its debt over the past few years.

The company currently has net debt of $1.5 billion, less than half of what it had in 2020, has no debt maturities through 2026, and is leveraged to less than 2x EBITDA.

Antero Resources

Going forward, the company’s strategy includes reducing total debt and allocating future free cash flow to share repurchases to further enhance shareholder value.

No dividends will be paid.

AR may not be all that appealing to income-focused investors, but it does have enormous free cash flow potential.

Analysts expect the company to generate $290 million in free cash flow this year under current market conditions, which is impressive given sluggish natural gas prices.

This represents 3% of the company’s market capitalization of $10.6 billion.

Next year, that figure is expected to grow to $1.1 billion, or more than 10% of its market capitalization.

If natural gas prices rise to $5 or more over time, the company could repurchase its shares at an unprecedented pace, significantly increasing the per-share value of the company.

Given the company’s free cash flow capacity at Henry Hub, we believe it could generate free cash flow yields of 12% to 16% in an environment of sustained high natural gas prices in the $4 to $5 range, depending on its growth plans.

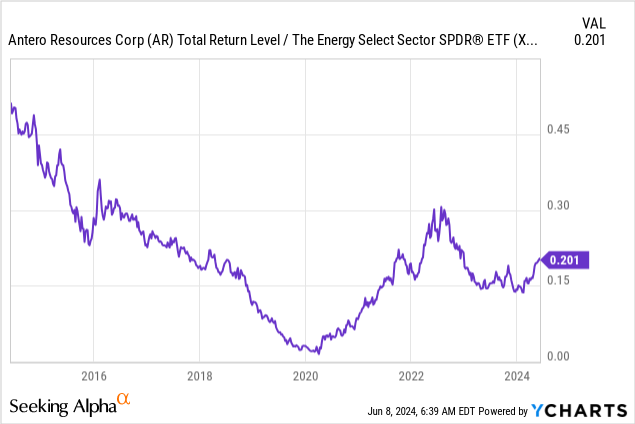

This is also because AR is a major player in the energy benchmark ETF (XL), because I believe the natural gas bull market is significantly undervalued.

Therefore, I Strong Buy I am downgrading AR as I expect the market to find it and its peers attractive, especially if global economic growth improves.

Personally, I have been holding AR shares since last year and have made a decent profit. However, I sold it as I was closing down my entire trading portfolio. For various reasons, I decided to move the cash into a long-term investment portfolio.

Now I’m considering how to most effectively incorporate non-dividend paying stocks into that strategy.

Needless to say, I really like AR and am looking to make it a “permanent” position in my long-term portfolio in the coming weeks and months.

So don’t be put off by the fact that we haven’t revealed a long position in AR at this time.

I invested in Antero Midstream, not Antero Resources.

remove

Driven by broader market trends such as growing AI-related demand, LNG exports, and the continued transition from natural gas to coal, the future for natural gas looks very promising.

Here, Antero Resources stands out as a top choice due to its superior efficiency, strategic positioning, and strong financial strength.

AR is well positioned to capitalize on growing global demand for natural gas with abundant Marcellus Basin inventories, low production costs and significant exposure to attractive LNG markets.

Additionally, the company has been focusing on reducing debt, which should generate significant free cash flow in the future, making it an attractive investment.

Pros and Cons

Strong Points:

- Strong inventory and efficiencyAR has had high-quality inventory in the Marcellus Basin for over 20 years and leads its peers in capital efficiency.

- Strategic PositioningAR is improving pricing by selling 100% of the natural gas from its own basins.

- Diverse product lineup: Large exposure to higher margin liquids and LNG will also improve pricing.

- Financial SoundnessAggressive debt reduction and strong free cash flow potential limit financial risk.

- Growth Tailwinds: AI, the transition from coal to gas, and the rapid rise in LNG exports are driving unprecedented demand growth.

Cons:

- No dividend: AR does not provide income through dividends.

- Market volatility: Natural gas prices are volatile, which makes AR much more volatile than the “average” stock you invest in.

- Industry Risk: Regulatory changes and environmental issues may affect our business and end markets.