Nastasia Samar/iStock via Getty Images

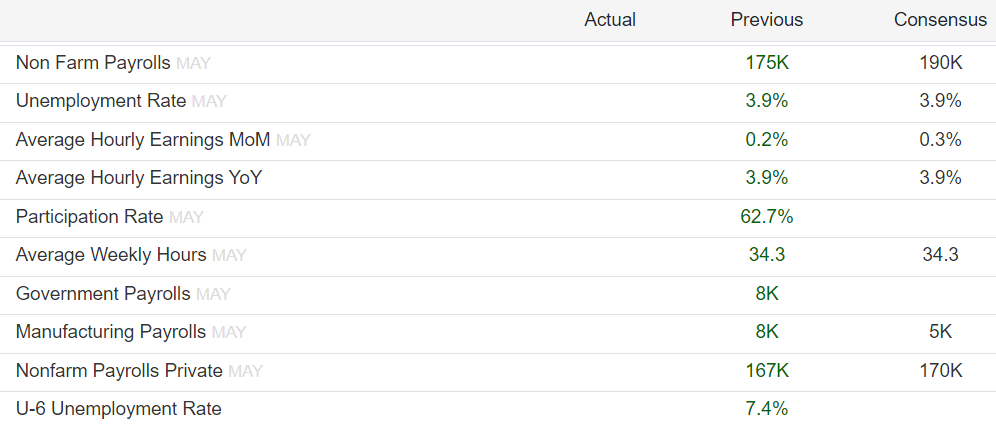

Key Labor Market Data

The employment report released on the first Friday of every month is always important, as the data often sets the direction for the rest of the month. As such, the stock market usually Huge reaction to the jobs report.

Last month’s April employment report was a very important one as it set the stage for the May employment report. The S&P 500 entered May in 5% down territory and with previous labor market data and “high” inflation readings for 2024, it was expected that the Fed would not make any significant rate cuts in 2024.

Actual employment data for April came in much weaker than expected, with 175,000 new jobs created compared to the expected 243,000. Additionally, wage growth was also weaker than expected. The forecast was for a 0.2% month-on-month decline. So as interest rates fell, the market began pricing in a Fed rate cut sooner than previously expected, and the S&P 500 soared to an all-time high in early May.

Technically, the 2-year futures (US2Y), 10-year futures (US10Y), S&P 500 (Spocks) all crossed their 20-day moving averages on May 3rd when the jobs report was released. Here is a chart of 2-year Treasury futures which sparked the rally on May 3rd when the jobs report was released. The peak came just after the CPI data on May 15th and the drop came after an unexpectedly strong flash PMI on May 23rd.

2 Year Futures (bar graph)

Two-year Treasury note futures are currently at the 20-day DMA level pending the release of the May employment report, which specifically suggests that there is roughly a 60% chance that the Fed will cut rates in September.

May Labor Statistics Forecast

Market consensus forecasts are for the labor market to strengthen slightly in May compared to April, but still be weaker than in the first quarter of 2024.

Specifically, the market is expected to add 190,000 new jobs, with the unemployment rate remaining at 3.9%, while wage growth is expected to remain strong at 0.3% month-on-month.

Expectations for May (Trading Economics)

Let’s guess the number

Clearly, the ability to predict actual numbers versus expectations would be a huge advantage in trading the S&P 500 in the short term.

So what information about the current state of the labor market can help us predict the actual numbers? Back to the April report: That was his weak spot.

- Government Employment: The government created just 6,000 jobs in April, well below the levels of the previous months (72,000 in March and 55,000 in February). This figure alone explains the difference between actual and expected.

- Leisure and Hospitality: This cyclical sector added just 5,000 new jobs in April, well below the 53,000 new jobs created in March.

The question then becomes, will the weakness in these two sectors continue into May?

Now let’s look at some key early data that can forecast May’s jobs report.

- Weekly unemployment claims: Initial claims spiked to 232,000 on May 4, but that was the peak and the numbers have declined in the weeks since. This suggests some weakness in the labor market, but overall the labor market remains tight.

- The S&P Global U.S. Composite PMI was released on May 23rd. This is a flash report, meaning the first data estimate for May. The PMI reading was a very strong 54.4, well above expectations, indicating that both services and manufacturing activity recovered in May. In terms of the employment situation, the report stated:

Although job cuts continue, the pace of job losses has slowed as companies have become more confident about next year and orders have increased.

As mentioned above, the main trigger was the release of the S&P Global US Composite PMI on May 23, which suggested that the May data would be stronger than the April data, causing interest rates to rise and stock prices to fall.

On the employment front, the S&P Global U.S. Composite PMI also indicated some weakness in the labor market, but suggested conditions were improving.

So, given what we know from these reports, it’s reasonable to expect payrolls to be just over 175,000.

However, the “good May” theme is already facing serious challenges. Specifically, the ISM manufacturing index fell more than expected in May, and new orders fell to 45, which would signal a recession. However, employment was 51, well above expectations. As new orders suggest, the market is starting to price in a possible recession; note how 2-year Treasury yields spiked after the ISM manufacturing index was released.

So in my opinion, given the amount of weaker than expected data, a negative surprise, i.e. the actual number being below 175,000, is more likely, which would result in my forecast of employment rising to 150,000 and unemployment to 4%.

Implications

The first part of the challenge is to predict the actual salary data. The second part is to predict the stock market reaction.

Let’s start with the assumption that the actual number will be slightly lower than expected, perhaps 150,000. In this situation, 2-year Treasury futures will rise and short-term interest rates will fall. As the bond market begins to price in an economic slowdown and ultimately a recession, long-term interest rates will fall as well.

S&P 500 (SP500In this situation, stocks could 1) plummet as the likelihood of a recession increases, or 2) rise as interest rates fall in anticipation of a rate cut by the Federal Reserve.

In my opinion, in this situation the S&P 500 would fall. Typically the stock market falls with the first interest rate cuts if there are signs of an impending recession, and I think that is exactly what is happening now.

This theory is supported by the reaction to the June 3 ISM manufacturing report, which showed that the cyclical Russell 2000 (International Hydrology) reversed its early gains and fell, while the Dow Jones (Diamonds). S&P 500 (spy) also fell, but closed higher as the meme fever spread to megacaps, especially Nvidia (NVDA). Nvidia can’t sustain the entire market forever, and eventually this bubble will burst too.

There will be enough data by Friday that this could change. More importantly, the CPI report will be released after the jobs report, and the worst case scenario is that the labor market weakens (as I expect), but inflation does not ease. This is the consensus at this point, given that core CPI is expected to rise 0.3% in May. Unfortunately, the data points in this direction: stagflation.