Adam Galt

Investment Thesis

Church & Dwight Co., Ltd.New York Stock Exchange:C.H.D.) is expected to continue to see revenue growth driven by increased promotional spending, expanded international distribution through the recent acquisitions of fast-growing businesses Hero and TheraBreath, and benefits from strategic bolt-on M&A. Revenue growth should moderate as CHD follows through on last year’s price increases and pricing advantages fade. The company’s margins should benefit from volume leverage, productivity improvements, and mitigating inflation, while declining pricing advantages and higher promotional expenses should be headwinds. The company’s stock is already trading slightly above its historical P/E, and I don’t see much room for upside from current levels. Therefore, I rate CHD stock Neutral.

Church & Dwight Revenue Analysis and Outlook

my Previous article Last year, I discussed the company’s strong growth prospects. Rising prices, eased comparisons, and improved fill rates. The company has reported strong growth since then. Last month, CHD reported its first quarter fiscal 2024 earnings, which showed similar trends.

In the first quarter of fiscal 2024, strong volume growth and the impact of past price increases also contributed to revenue growth, which helped offset headwinds from the sale of MEGALAC, part of the animal nutrition business within the Specialty Products segment, as well as weakness in the flosser and gummy vitamin categories due to lower consumption.

The company’s total sales increased 5.1% year over year to $1.5 billion. Excluding a 0.3 percentage point benefit from favorable foreign exchange and a 0.4 percentage point headwind from divestitures, organic sales increased 5.2% year over year. Organic sales growth reflected a 3.7 percentage point benefit from increased volume and a 1.5 percentage point benefit from favorable price/mix.

On a segment basis, Consumer Domestic achieved revenue growth of 4.3% year over year on both a reported and organic basis, benefiting from higher prices and volumes driven by market share gains and stronger demand. Consumer International also benefited from higher prices and volumes driven by market share gains from continued expansion in international markets, resulting in 10.6% year over year sales growth on a reported basis and 8.8% year over year sales growth on an organic basis. Finally, Specialty Division achieved sales growth of 1% year over year on a reported basis, and excluding headwinds from the MEGALAC divestiture, organic sales increased 7.2% year over year driven by higher prices and volumes driven by improving demand and easing competition.

CHD’s past sales (Corporate data, GS Analytics Research)

CHD’s past company-wide organic sales analysis (Corporate data, GS Analytics Research)

Going forward, we expect the company to continue to grow over the next few quarters. Management is looking at increasing promotional spending in the coming quarters, which should translate into sales growth. Management is targeting marketing spending to be around 11% of sales in FY24, up from around 10.9% in FY23, but still 70-80 basis points below pre-COVID levels. As inflation headwinds abate and gross margins return to normal levels, we expect a portion of the increased gross margins to be reinvested in marketing, with marketing spending returning to pre-COVID levels translating into sales growth.

Marketing costs in 2024 (CHD’s dbAccess Global Consumer Conference 2024 presentation slides)

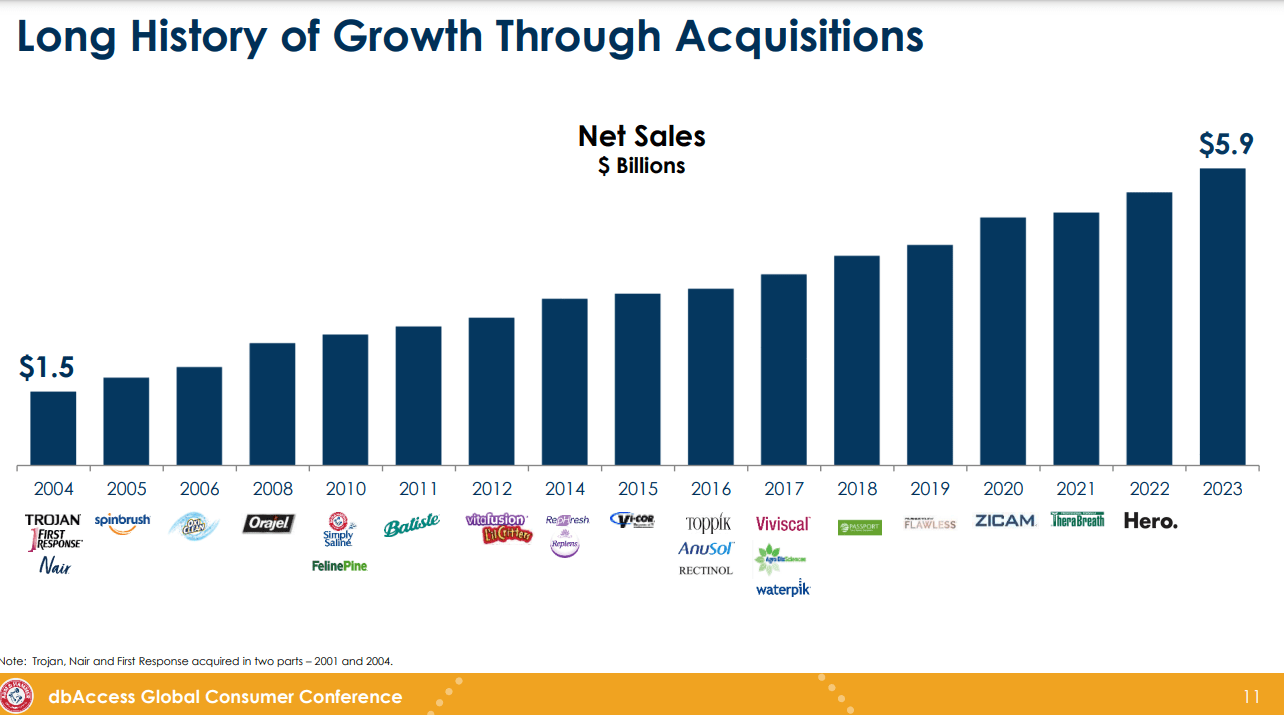

The company has seen good volume growth over the past few quarters and is expected to continue this trend going forward. The company has benefited from increased distribution from its recent fast-growing acquisitions of TheraBreath and Hero and is expected to continue to grow, especially internationally, over the next few years. The company’s strategy is to acquire smaller, faster-growing brands and expand distribution by leveraging its existing domestic and international networks. With the company’s net debt to TTM EBITDA ratio currently at around 1.6x, more such bolt-on M&A is likely in the future, which should aid the company’s sales growth.

CHD’s M&A history (CHD’s dbAccess Global Consumer Conference 2024 presentation slides)

However, the downside is that the pricing benefits the company has enjoyed in recent years will no longer contribute significantly to its top line. The company should finish most of the price increases implemented in response to post-COVID inflationary conditions in 2Q24, and pricing growth should contribute negligible amounts to top line going forward. Thus, while organic revenue growth should remain positive, supported by volume growth, the pace of growth should slow in coming quarters as the benefits of pricing contribution fade.

Church & Dwight Margin Analysis and Outlook

In the first quarter of fiscal 2024, the company’s margins benefited from the carryover effect of higher prices and favorable mix, which together increased 130 bps year-on-year. Margins were also boosted by a 130 bps year-on-year benefit from productivity improvements and an 80 bps year-on-year benefit from lower transportation costs due to less inflation compared to the same period last year. This more than helped the company offset a 110 bps year-on-year headwind from higher manufacturing costs and a 10 bps year-on-year headwind from unfavorable foreign exchange. As a result, gross margins increased 220 bps year-on-year to 45.7%.

However, adjusted operating margin decreased 10 basis points year over year to 20.8%, as the benefit of increased gross margin was offset by an increase in selling, general and administrative expenses as a percentage of sales compared to the same period last year.

CHD’s historical gross profit and adjusted operating profit (Corporate data, GS Analytics Research)

Going forward, the company’s margin growth should continue to benefit from improved productivity and easing inflation. However, with most of the price increases occurring in Q2 2024, the company will no longer benefit from the pricing carryover it enjoyed in previous quarters. As a result, gross margin improvement should shrink going forward. Additionally, management plans to increase promotional spending going forward, which should negatively impact operating margins.

Evaluation and conclusion

Church & Dwight is currently trading at 31.16 times the fiscal 2024 consensus EPS estimate of $3.46, which is slightly higher than its five-year average forward P/E of 29.26.

While the company is optimistic that it will continue to achieve revenue growth driven by increased marketing spend, expanding international distribution, and bolt-on M&A, the pace of organic growth should slow in coming quarters as pricing advantages fade. Additionally, productivity improvements and volume leverage should continue to drive margin expansion, but this should be offset to a significant extent by fading pricing advantages and higher promotional spend.

The stock is trading at a slightly higher level than the historical average, and the potential for upside from this level is not very strong, as the pace of organic growth is expected to slow. It is hard to justify a premium valuation compared to the historical average when organic growth is expected to slow. The FY25 EPS consensus estimate is $3.75 Apply the average PER(FWD) for the past 5 years. 29.26 timesThe price target is $109.73, which doesn’t offer much room for upside from current levels. I believe the company’s growth prospects are already priced into the current valuation. Therefore, I would stay on the sidelines and rate the stock Neutral for now.