SlavkoSereda/iStock (via Getty Images)

investment thesis

StoneX Group (Nasdaq:Nasdaq:snecks) has consistently grown revenue and profits over the past several years and continues to compound capital. StoneX has a high return on equity and a well-diversified business. We are impressed by its resilient growth and attractive long-term growth opportunities. Even at a fair valuation, I still think the stock is attractive given its track record of compounded capital and strong ROE. To me, StoneX seems like a great business at a fair price. Therefore, we rate this stock a buy.

Company Profile

StoneX aims to connect clients to all the markets they need to manage risk, strategically capture and trade opportunities, and address operational business needs. According to their strategy, annual report “To be the only trusted partner for our clients through our network, products and services.” Services that help you pursue trading opportunities, manage market risk, make investments, and improve performance. ”

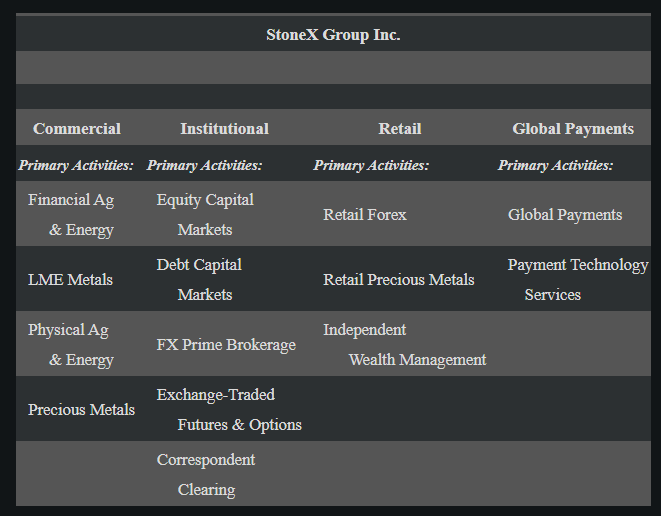

According to its annual report, the company is divided into four segments: commercial, institutional, retail, and global payments. With “over 54,000 commercial, institutional, and global payment clients and over 400,000 individual accounts in over 180 countries,” StoneX helps clients of all types by helping them trade more efficiently and strategically. We have a track record of providing value to

The commercial segment refers to “activities related to the identification, management, hedging and monitoring of various product and financial risks faced by commercial entities during the business cycle.” StoneX is a one-stop shop for commercial clients, providing risk management consulting solutions, execution and clearing services, and market intelligence and research.

The Institutional segment stands for “Liquidity with optimal execution, consistent liquidity across robust fixed income products, and competitive and efficient clearing on all major futures and stock exchanges worldwide. and a complete suite of stock trading services to support execution. As a prime brokerage for stocks and major foreign currency pairs and swaps. ”

The Retail division provides retail clients around the world with access to over 18,000 global financial markets, including spot foreign exchange, CFDs (investment products that provide returns linked to the performance of the underlying assets), financial trading and spot investments. The goal is to do. “Precious metals”.

Global Payments “provides customized payments, technology, and financial services to banks, commercial enterprises, charities, NGOs, and government agencies.” We assist our clients with foreign exchange and currency exchange, with a focus on facilitating cross-border payments securely and effectively.

10-K

As a diversified financial services company, StoneX plays a central role in helping customers trade smartly and manage risk prudently. I think of it as a giant matchmaker with many built-in solutions to establish a name in the financial field and become a true one-stop shop for all the trading needs of our customers. I like this business and believe the value they provide is substantial, judging by the company’s consistent underlying growth.

Strong Q2 earnings strengthen growth story

On May 8, 2024, the company announced what I believe to be excellent numbers for second quarter earnings, reinforcing my belief that the company’s consistent growth should continue.According to this press release,

Quarterly operating revenue $818.2 millionUp 16%

Quarterly net income $53.1 million,ROE 14.0%

Quarterly diluted EPS $1.63 increase per share twenty five%

The majority of this growth was driven by retail and institutional, where operating revenue increased 30% and 28%, respectively, year-over-year. Management believes this is due to “diversification of our product offering and customer base” and I suspect they have come up with new products to attract new customers to further grow the business. I’m thinking about it.

Return on equity continues to be strong; transcript It says, “ROE on tangible assets is 14.8% and ROE on nominal book value is 14%, which, just to be clear, has increased by 53% over the past two years, and both metrics are in line with our long-term goals. We believe we can maintain ROE at around 15% over the long term due to our track record of creating innovative new products to retain customers and diversify our offerings. Therefore, investing in StoneX is like investing your money in a fund that compounds your capital at 15% every year, which is very attractive to me. In my opinion, even with a fair valuation, the return an investor receives will be close to the actual ROE the company earns over the long term.

The retail segment was the highlight of the quarter in my view, with management detailing its growth on the earnings call.

Segment profits increased in all segments compared to the same period last year. This was led by the retail segment, which increased by 127%, followed by the payments segment, which increased by 24%.

I believe the retail segment is gaining momentum and will become more important in the growth story, as I view the commercial segment as relatively saturated and mature at this point. Interestingly, his StoneX website respectfully refers to retail investors as “voluntary customers” and offers them physical investments in precious metals. I see StoneX Bullion (the company’s physical precious metals business) as particularly attractive in today’s market as it could be used by many investors as a hedge against inflation. At the end of the day, I think management has been very innovative in terms of expanding their product offerings and coming up with new ideas to reach new customers, especially retail.

Strengthen customer retention with a one-stop shop

In my opinion, the mandate to provide a one-stop solution to customer needs has increased lock-in and made it more difficult to switch to other service providers. The main competitive advantage I see here is switching costs. Because clients rely heavily on his StoneX back office and trading services and cannot easily leave StoneX.

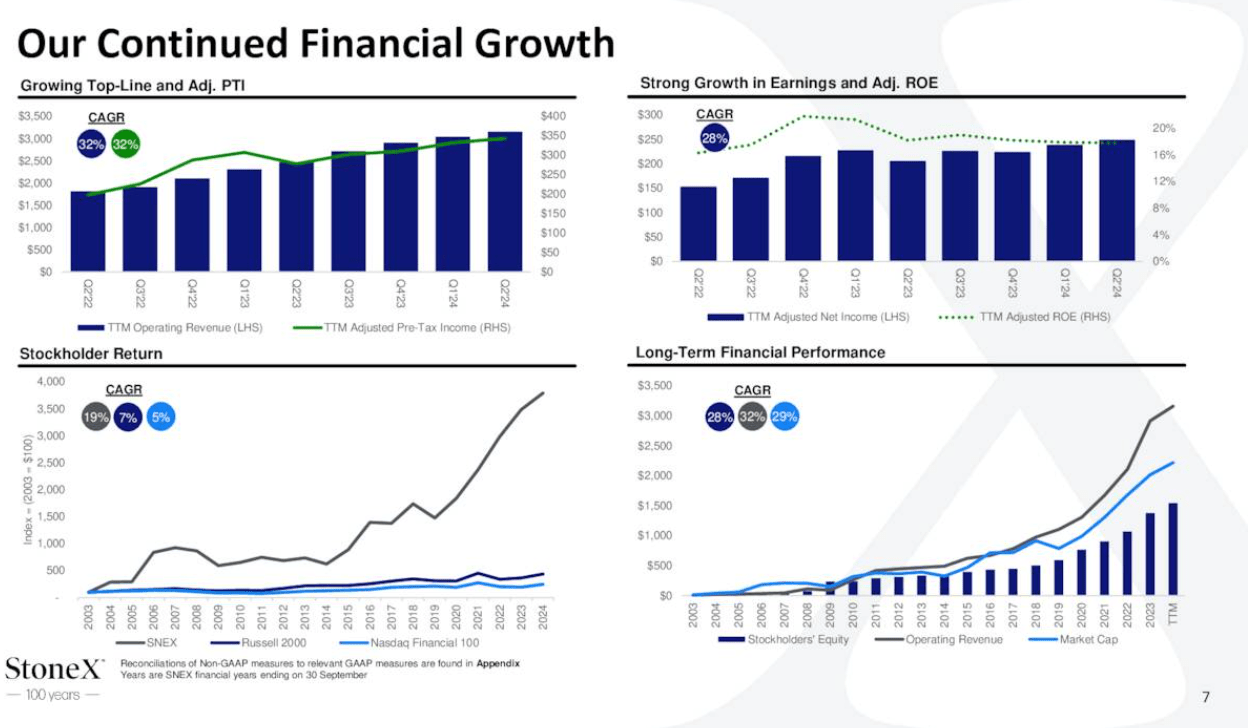

Supporting this claim, their presentation shows significant growth every year without any issues.

Investor presentation

A company that continues to generate stable profits and ROE requires a certain degree of competitiveness. I believe that the combination of high lock-in and attractive unit economics makes this business a very profitable and fast-growing company. As a service company, the company is able to earn very attractive spreads and commissions based on market activity and has a flexible cost structure that fluctuates primarily based on trading volume. Therefore, according to the presentation, operating revenue has increased linearly even during the pandemic crisis, demonstrating the company’s resilience to economic shocks.

I think the graph at the bottom right of page 7 says it all. In my view, over the long term, stock prices always follow fundamentals, with market capitalization closely tracking operating income and capitalization. Assuming the company can strongly retain customers, innovate new products, and diversify its customer base, the stock should continue to track operating revenues in an orderly manner. StoneX seems to be very resilient to economic fluctuations, and oil prices, pandemics, interest rates, and inflation don’t seem to be able to stop StoneX from rising. Financial service providers provide risk management and hedging tools to protect their clients from market volatility, so they need to actually profit from this volatility.

Evaluation – long-term compound machine

Because I believe that buying a great long-term compounder at a fair price is actually a deceptive bargain, even if the multiple is in line with the sector median, Evaluation can be difficult. What I’m saying is that while it may not look cheap, if investors factor in the growth and high return on equity, it’s a good idea to buy this stock at a respectable multiple. Therefore, we do not use a “target price” here as we believe investors should buy and hold this name as long as the fundamentals grow.

Assuming that revenue continues to rise at a 15% CAGR over the next few years, we would expect the stock price to follow suit. With a 10x diluted EPS of $7.50, the stock trades at a fair price, but strong retail and institutional growth and continued high ROE will likely result in a diluted EPS of around 10x over the next few years. We expect it to grow at a CAGR of ~15%. The company appears to be very resilient to economic shocks, so the stock should ultimately provide investors with a return of about 10% to 15% with relatively low risk.

Investor presentation

Long-term economic growth should drive StoneX forward as assets under management increase over time and more investors enter the market. There will always be risks that need to be hedged, trading activity will increase year on year, and StoneX’s fees and commissions should increase. I view this long-term compounding machine as a buy. This is because they have growth potential and high ROE, and are currently trading at fair prices.

risk

Reputation is important and StoneX must be careful in managing its business to maintain its brand. Compliance with regulations, continuous innovation to deliver better service, and a diverse customer base appear to be essential for this business to grow safely. StoneX requires all stakeholders with whom it does business to conduct business ethically and responsibly and to avoid harm to its reputation.

StoneX relies on continued market fluctuations to sell the derivatives needed to hedge this risk. In a way, volatility is a huge benefit for StoneX, as unless there are dramatic changes in commodity prices, demand for StoneX’s hedging services may decline as people won’t need to hedge their risks. Investors should expect the market to remain volatile, but any government intervention regarding commodity price floors or caps could hurt StoneX’s fundamentals.

The industry remains highly competitive, with many products to choose from in terms of market makers and hedging solution providers. StoneX must continue to remain competitive on price and volume in order to attract new customers and grow its business. Additionally, StoneX must be aware of counterparty credit risk, as some customers may use margin for trading activities and may not be able to meet their margin obligations.

Buy StoneX

I think I found a great long term compounding machine that trades at a fair price. I think long-term shareholder return roughly approximates a company’s actual return on equity over the long term (15%). So my expectation is that investors will earn 15% annually for as long as they own the stock. . Resilient to economic shocks and poised to benefit from price fluctuations, I view StoneX as a safe haven from market collapses and rate the stock a buy.